-

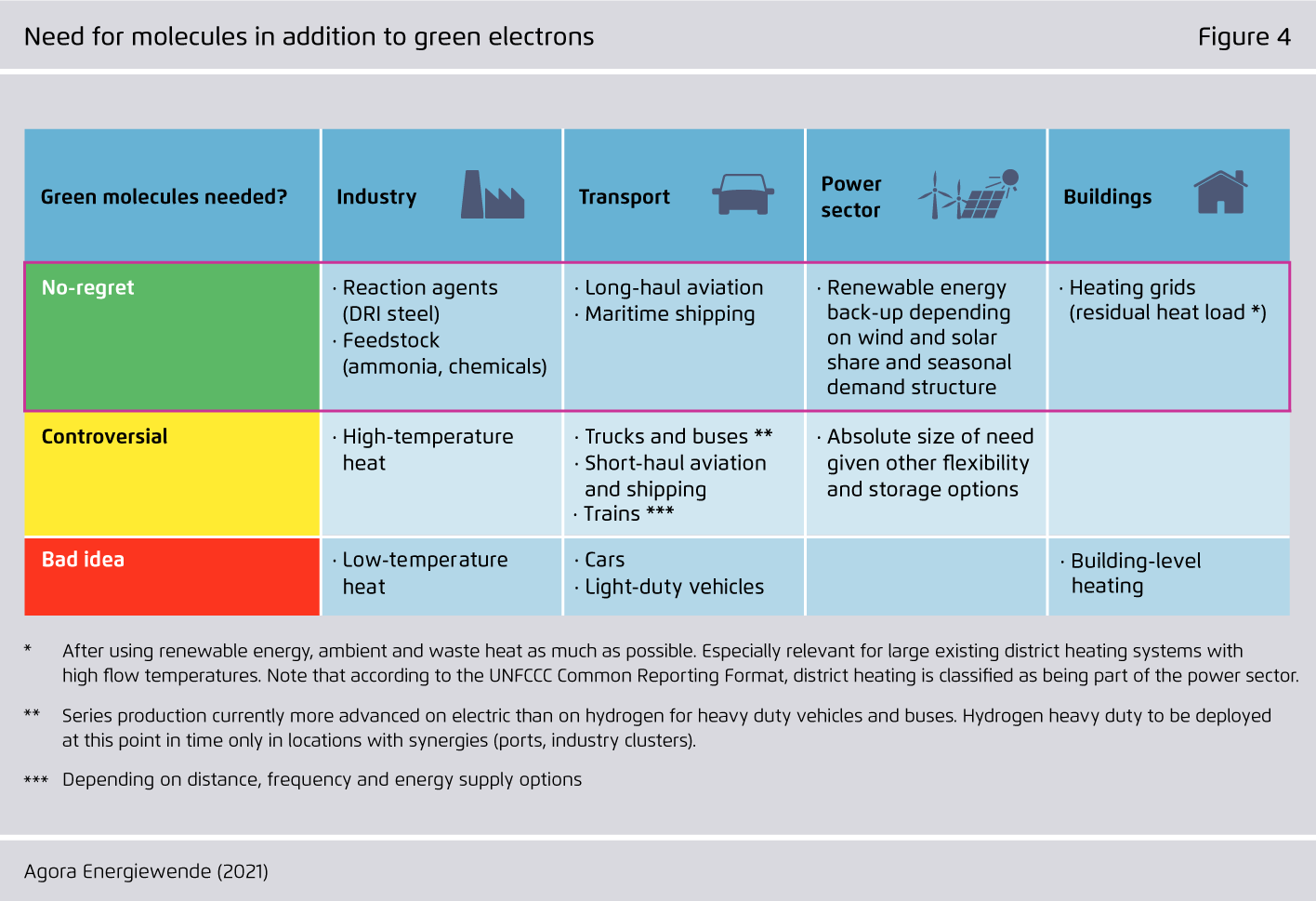

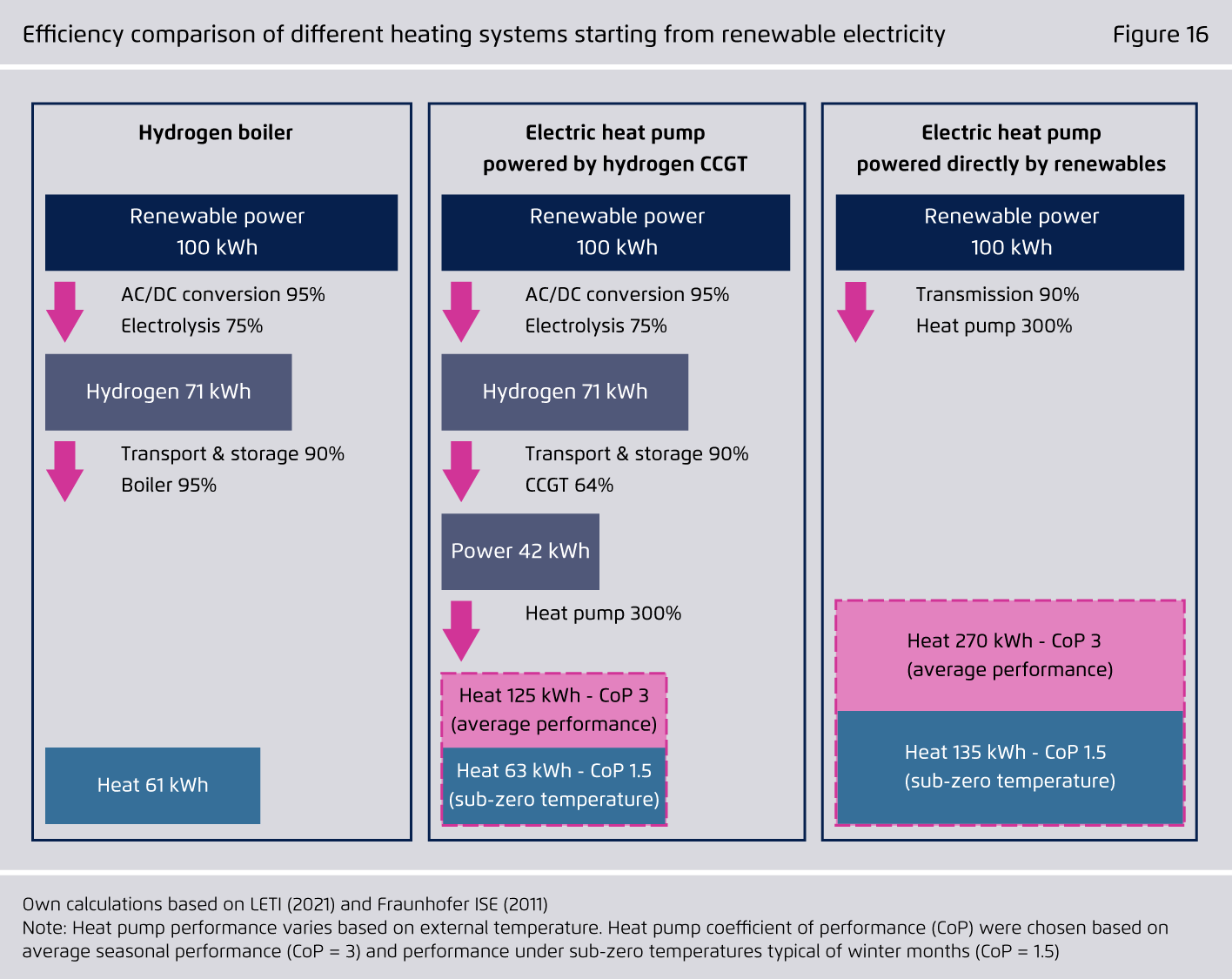

There is an emerging consensus that the role of hydrogen for climate neutrality is crucial but secondary to direct electrification.

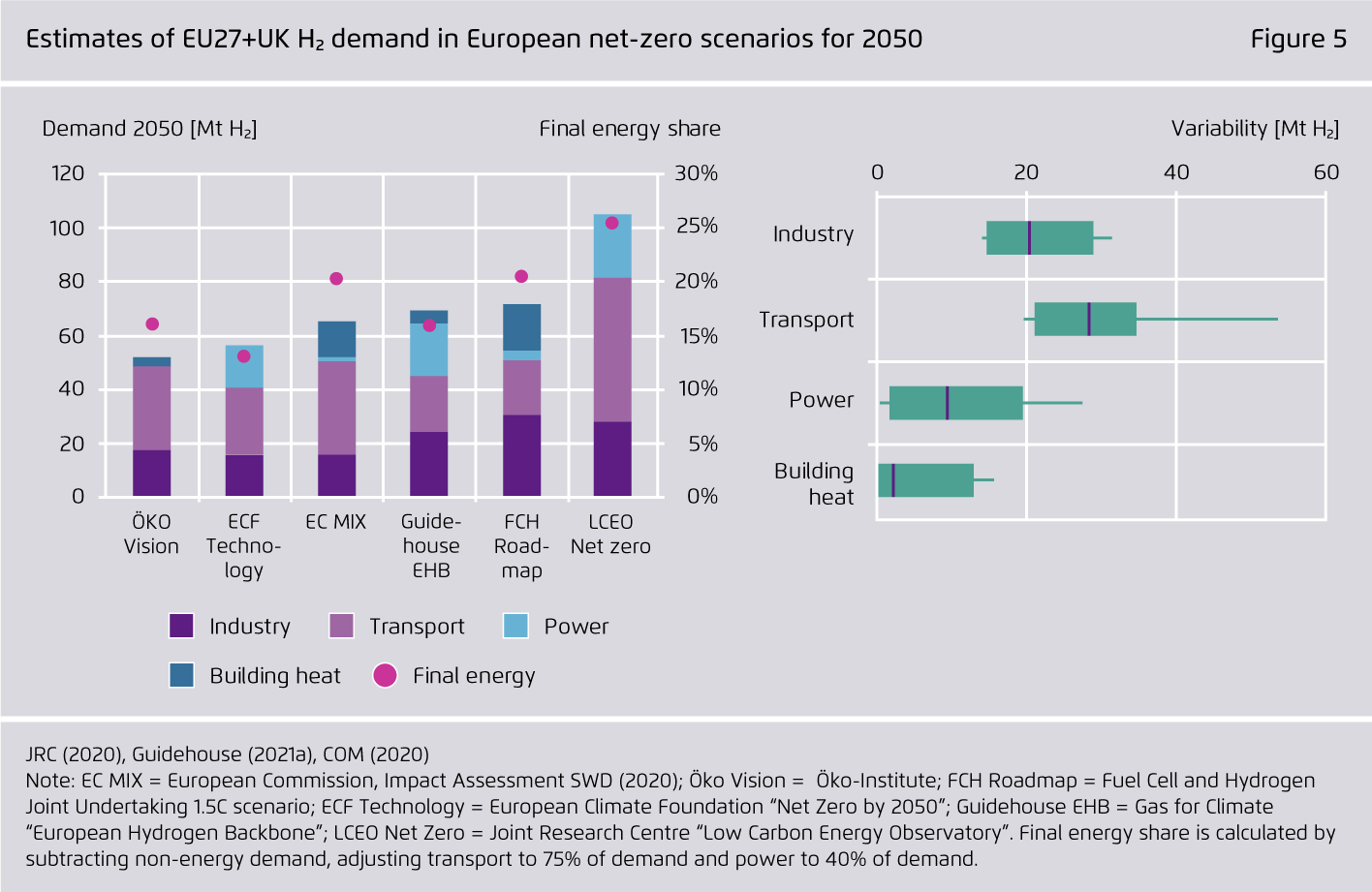

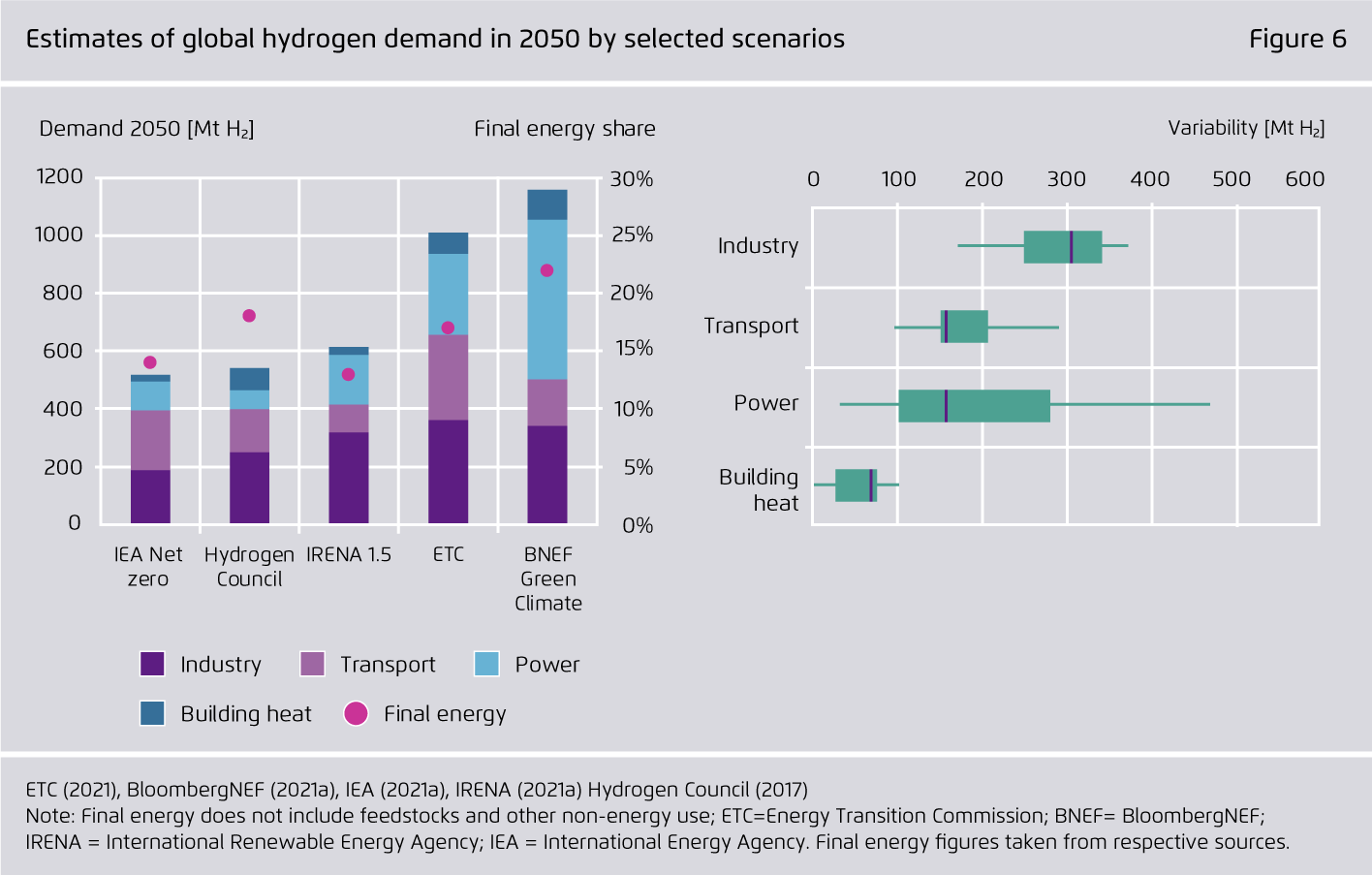

By 2050, carbon-free hydrogen or hydrogen-based fuels will supply roughy one fifth of final energy worldwide, with much of the rest supplied by renewable electricity. Everyone agrees that the priority uses for hydrogen are to decarbonise industry, shipping and aviation, and firming a renewable-based power system. Therefore, we should anchor a hydrogen infrastructure around no-regret industrial, port and power system demand.

-

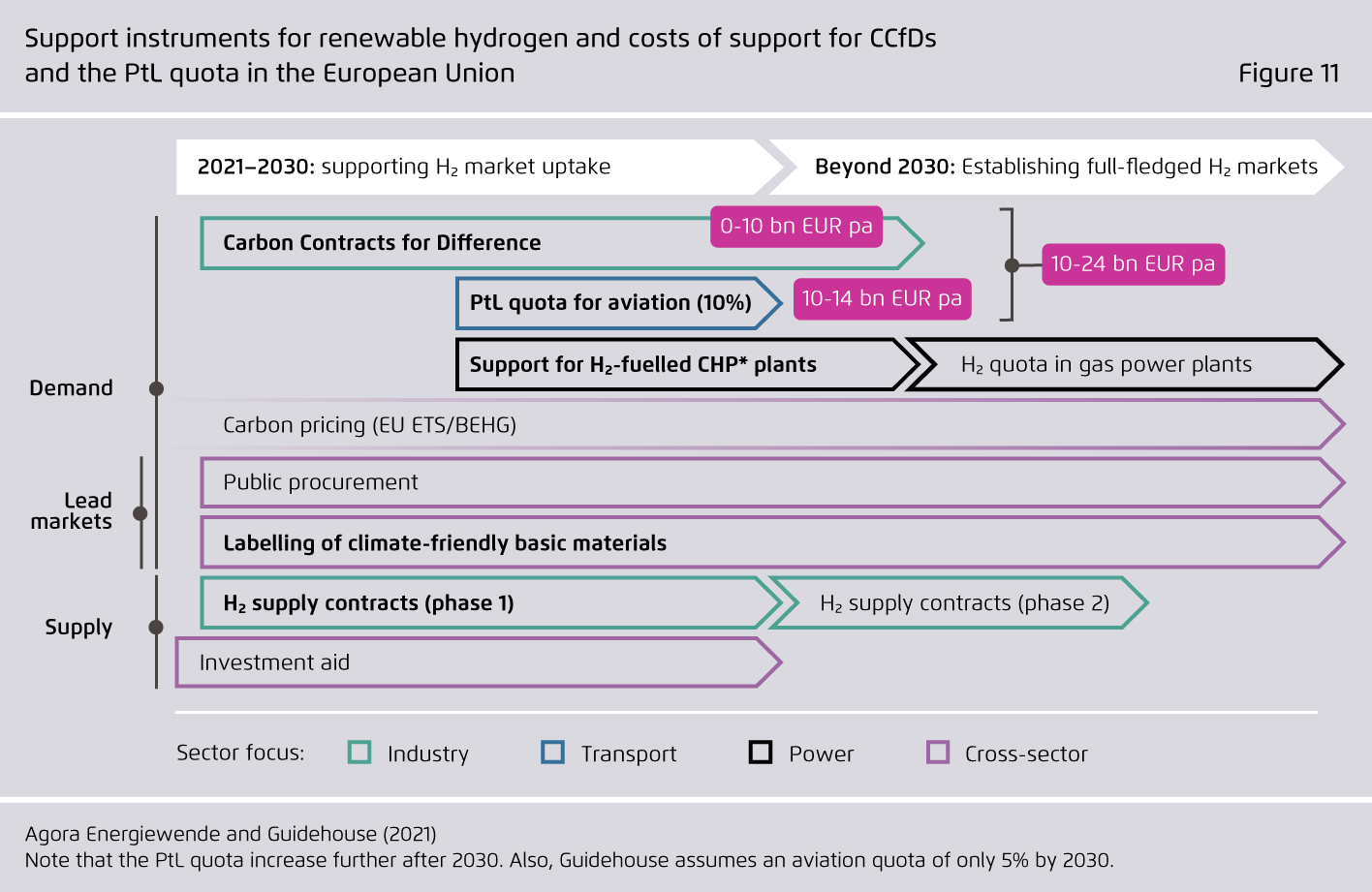

Financing renewable hydrogen in no-regret applications requires targeted policy instruments for industry, power, shipping and aviation.

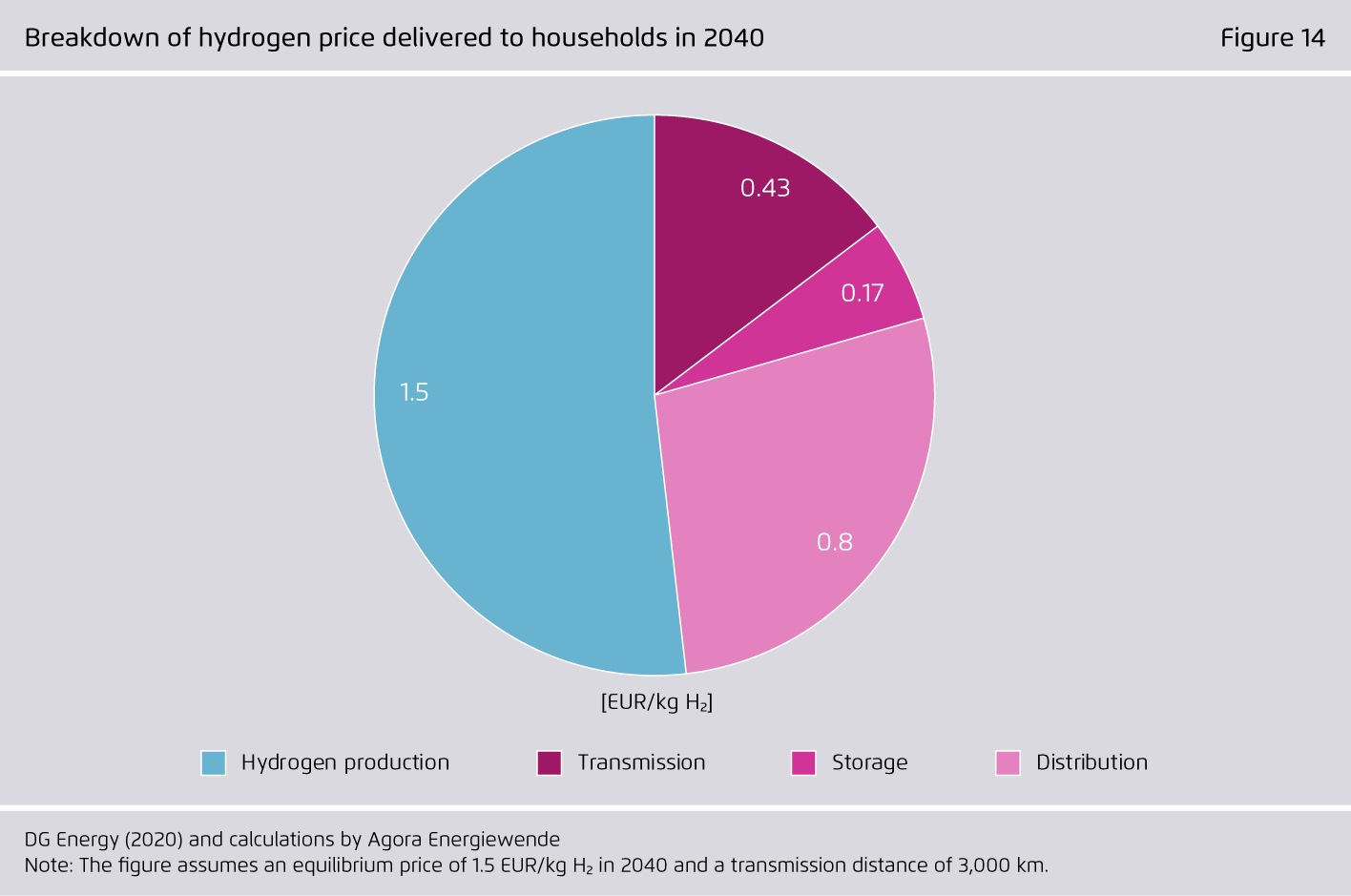

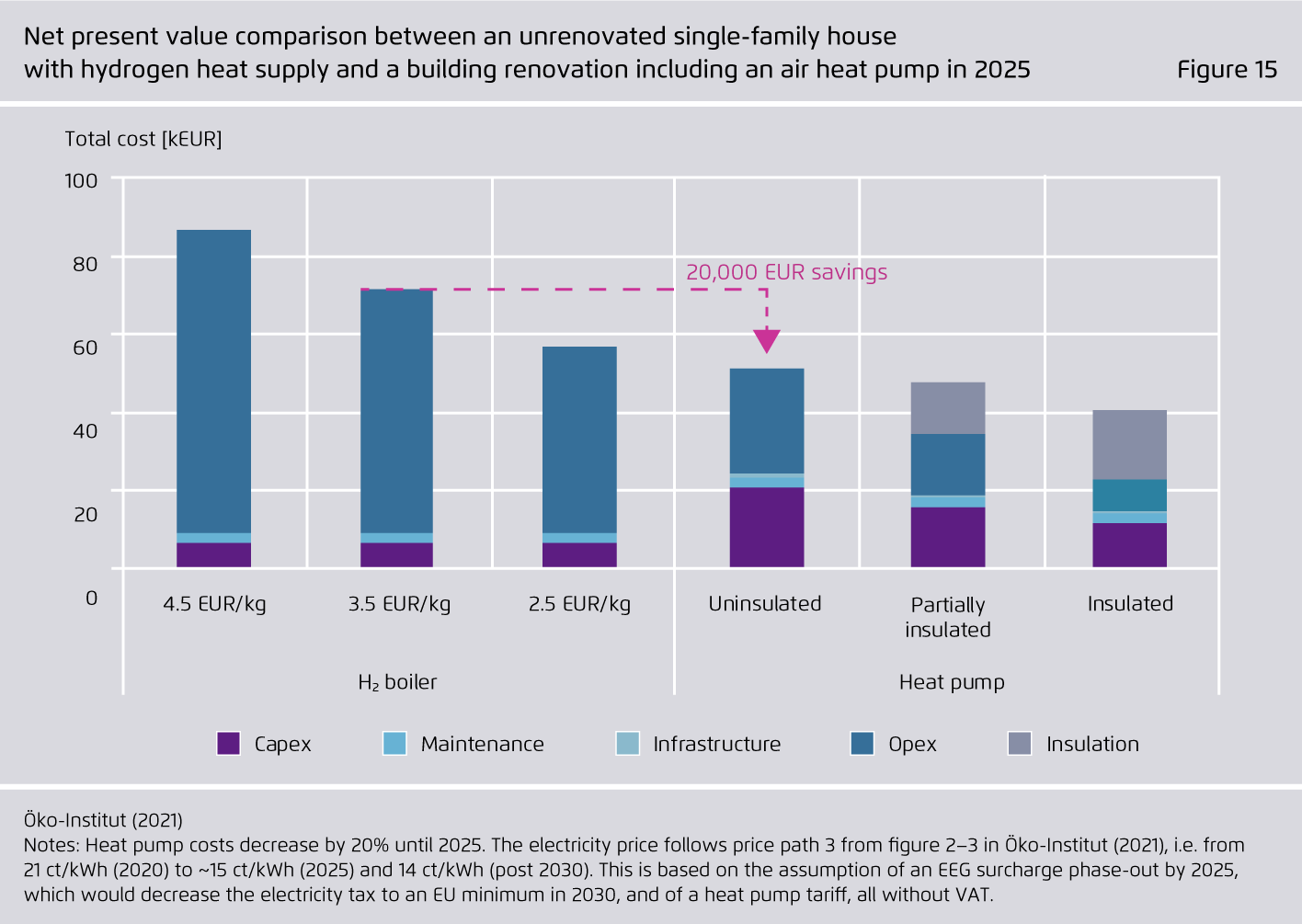

This is critical for incentivising hydrogen use where carbon pricing alone cannot do the job quickly enough. While policy options are available at a reasonable cost for industry, power and aviation, there is no credible financing strategy for hydrogen use by households. Blending is insufficient to meet EU climate targets and carbon prices high enough to deliver hydrogen heating would be unacceptable for customers.

-

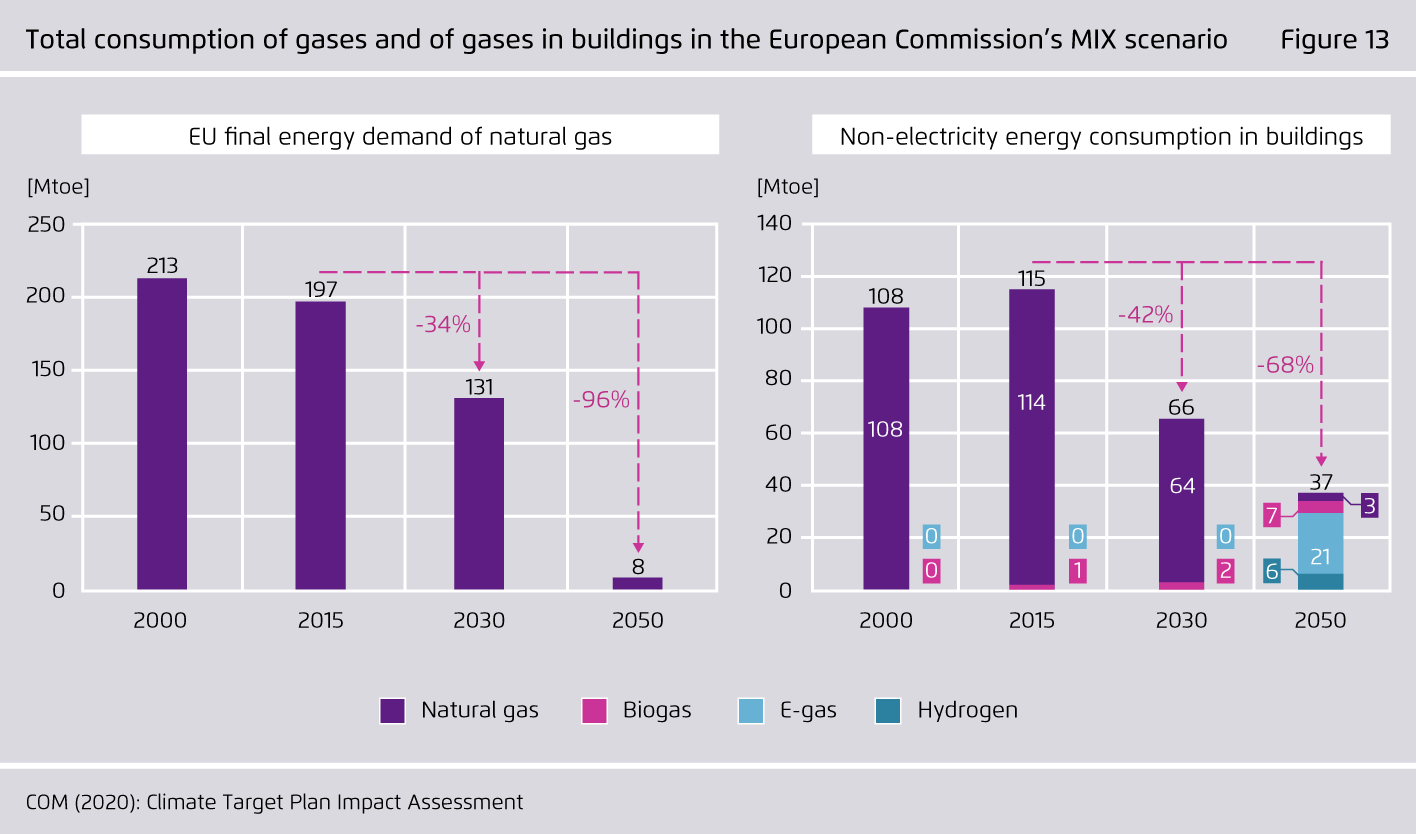

Gas distribution grids need to prepare for a disruptive end to their business model, because net-zero scenarios see very limited hydrogen in buildings.

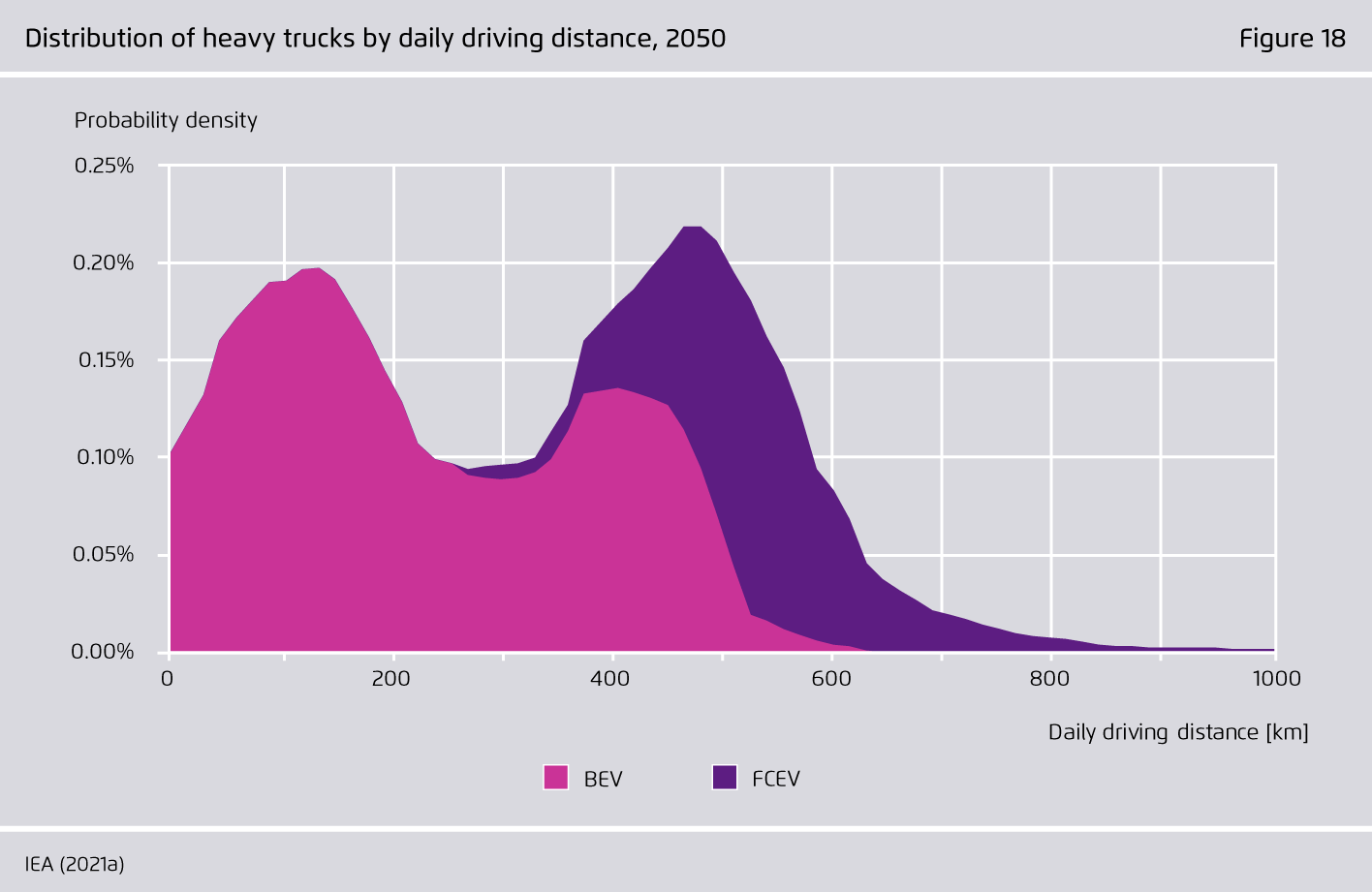

To stay on track for 1.5C, Europe needs to reduce consumption of natural gas in buildings by 42 percent over the next decade, as per the EU Impact Assessment. Similarly, land-based hydrogen mobility will remain a niche application. Any low-pressure gas distribution grids that survive will be close to ports, where refuelling and storage infrastructure could provide an impetus for the decarbonisation of the maritime and aviation sectors.

-

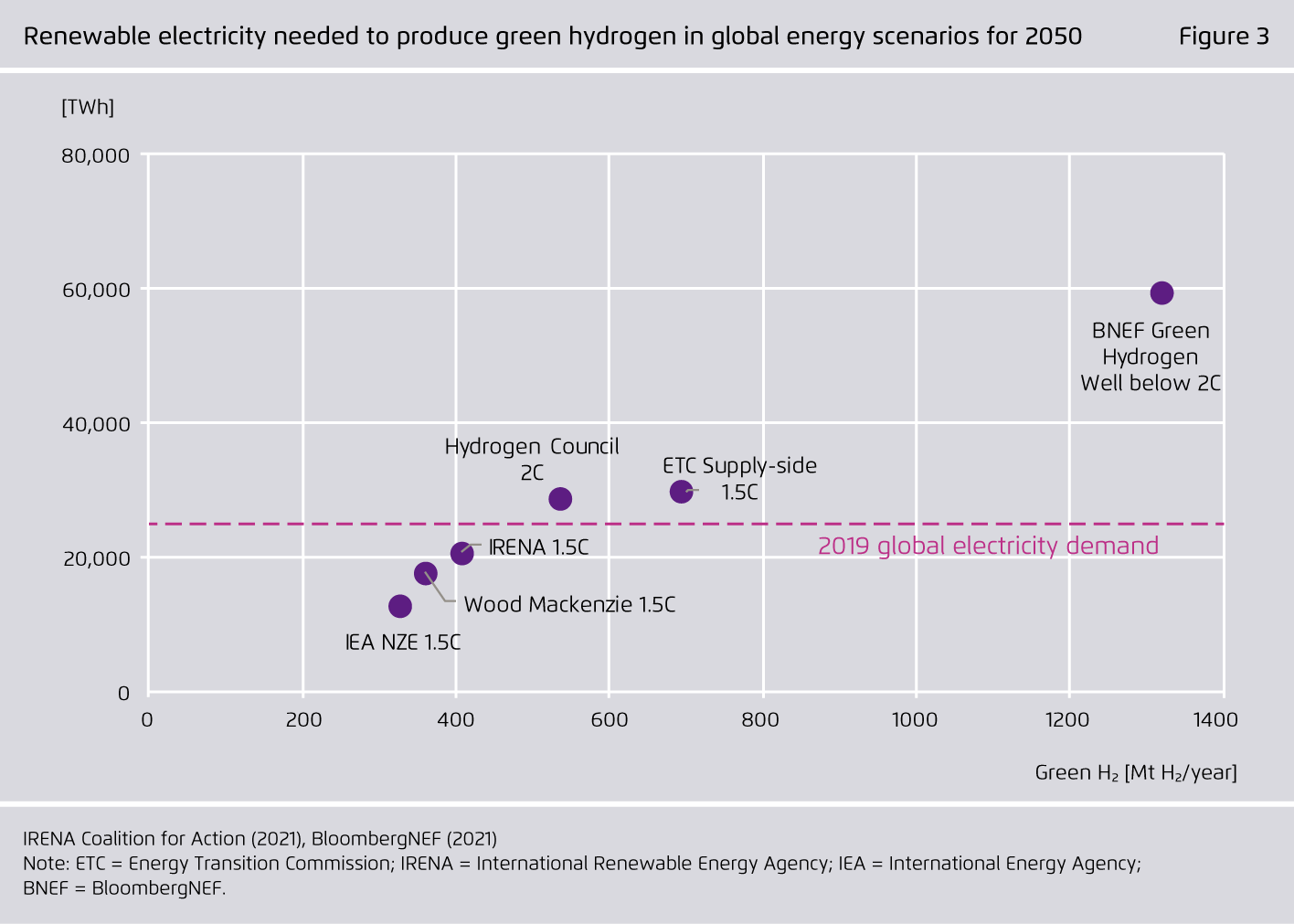

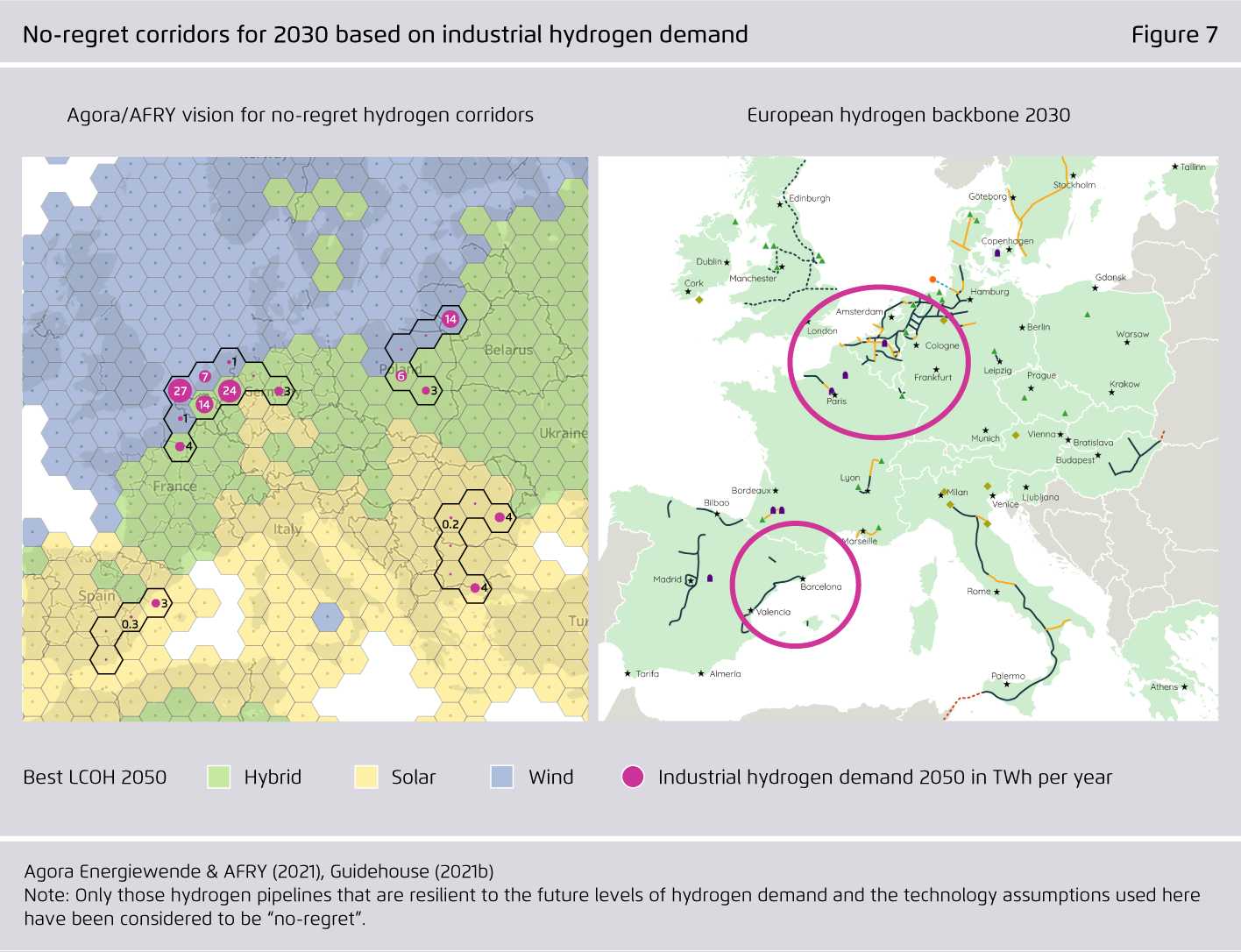

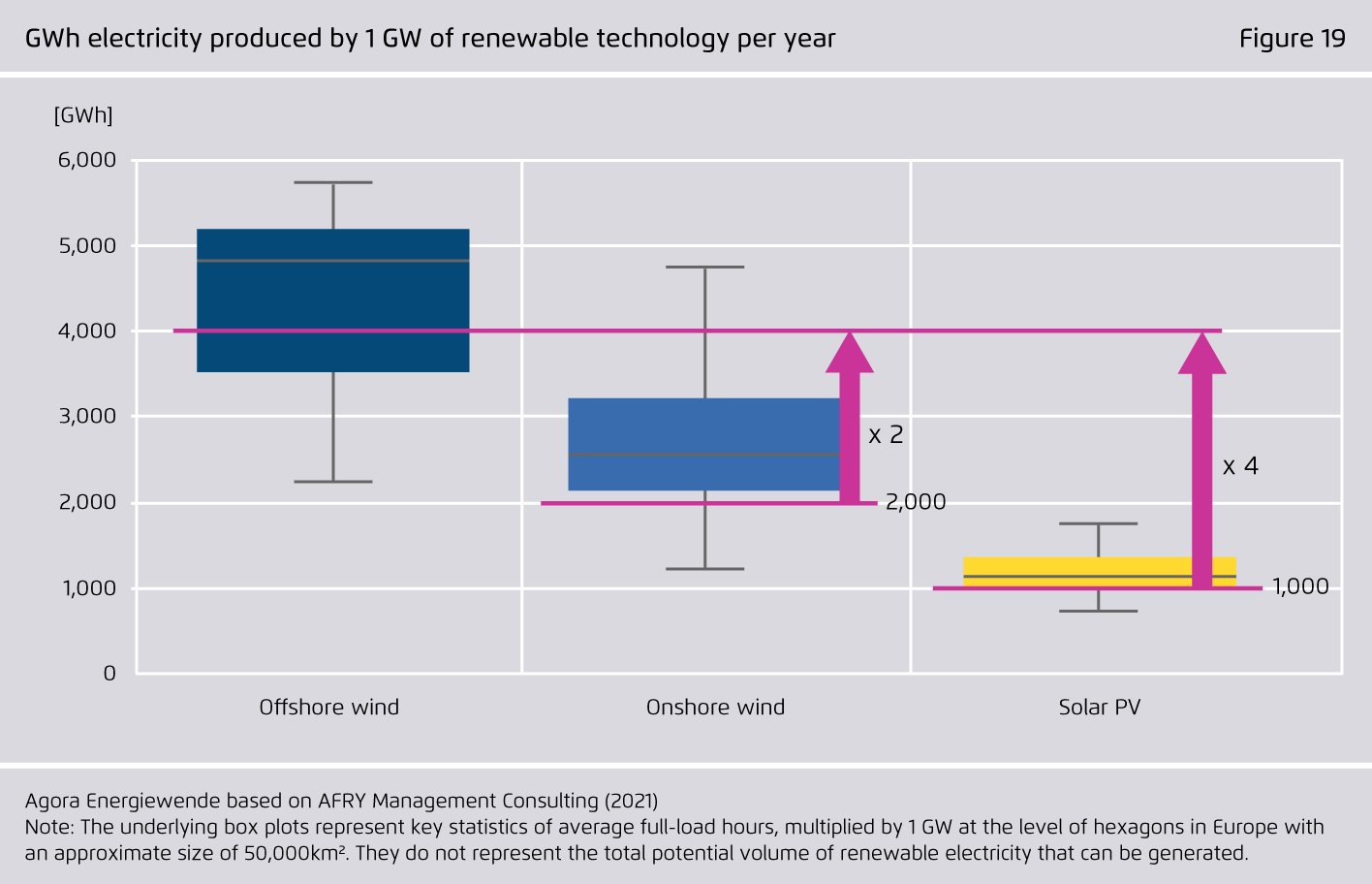

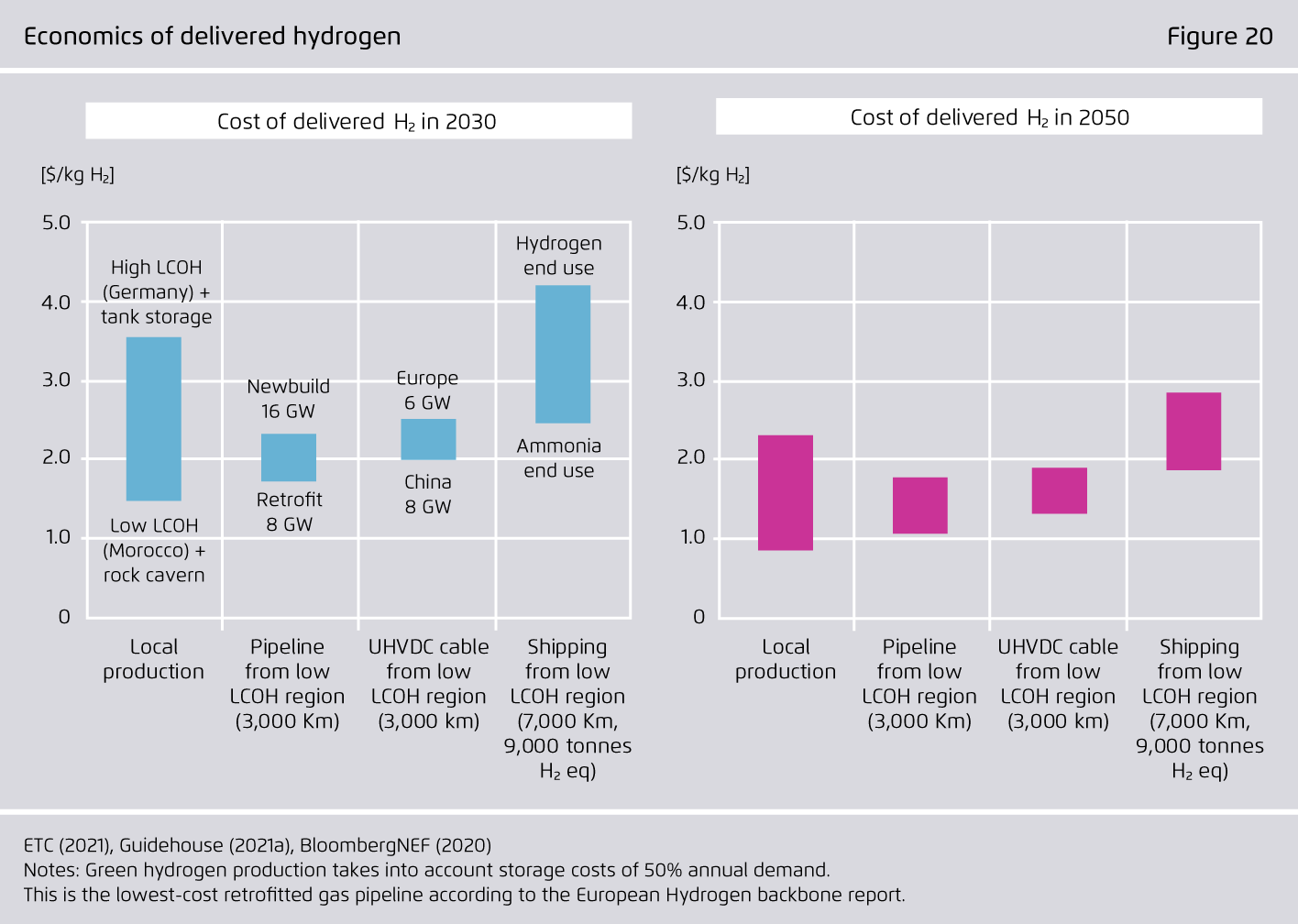

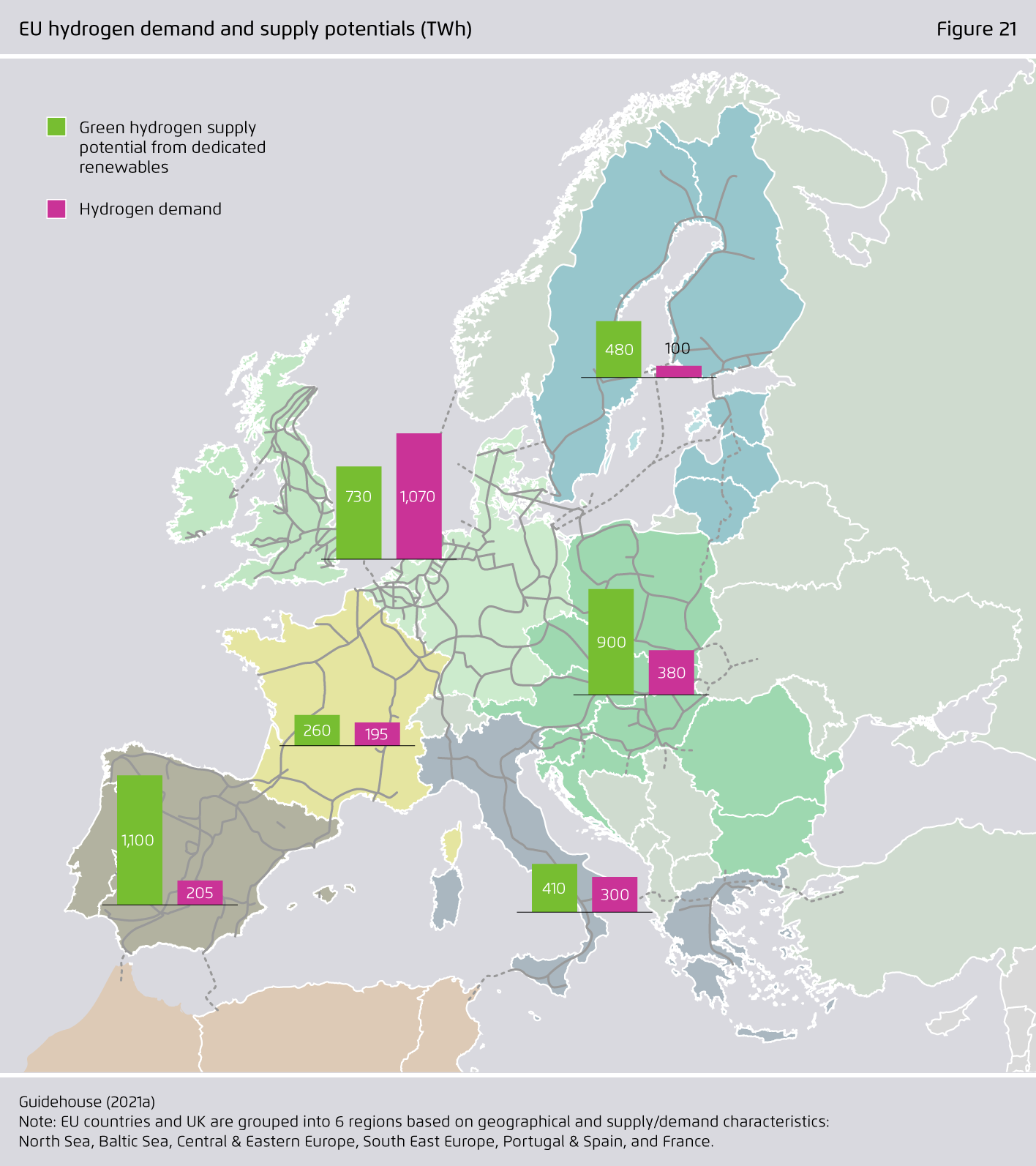

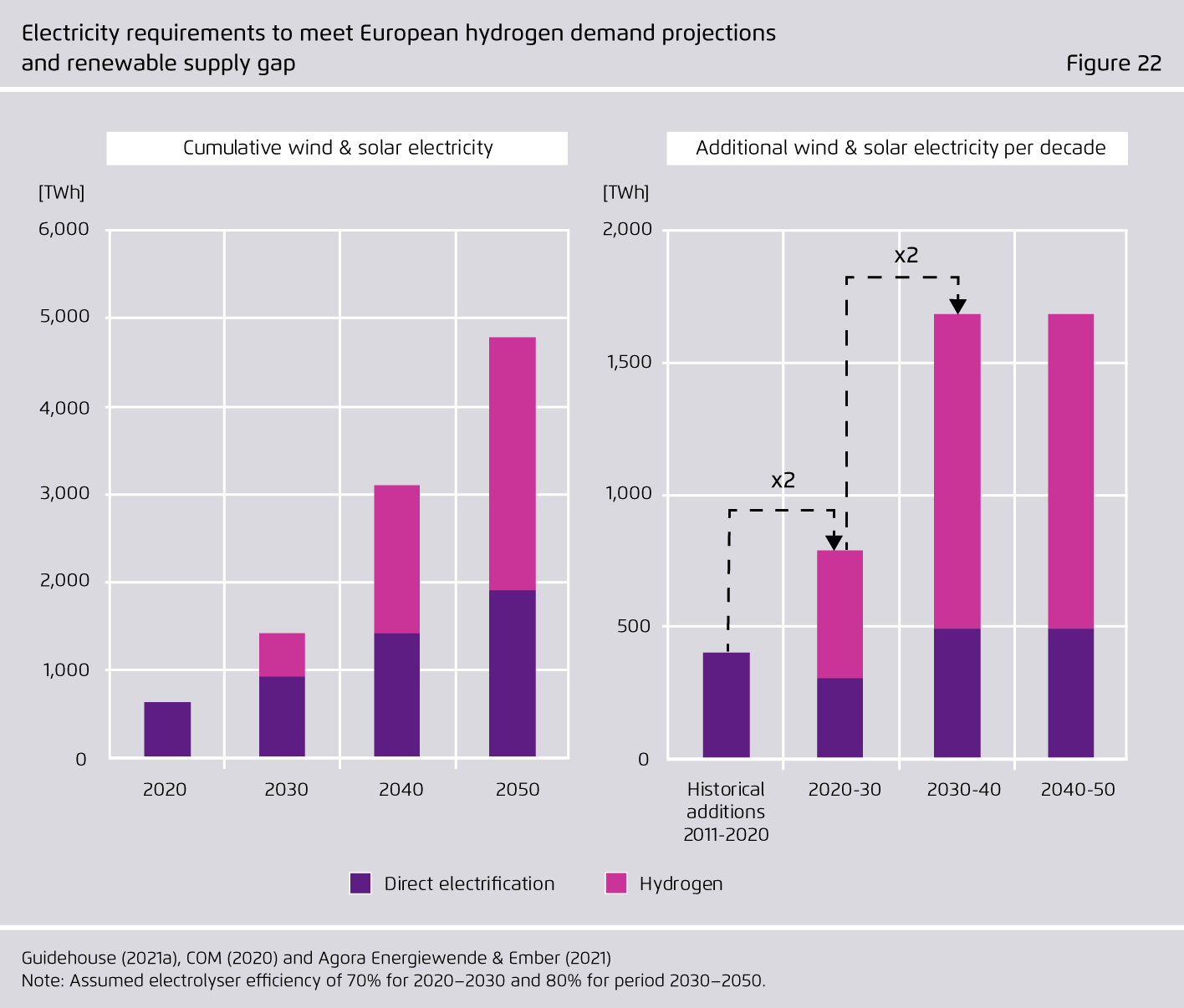

Europe has enough green hydrogen potential to satisfy its demand but needs to manage two challenges: acceptance and location of renewables, as each GW of electrolysis must come with 1-4 GW of additional renewables.

To keep industry competitive, the EU should therefore access cheap hydrogen (green and near-zero carbon) from its neighbours via pipelines, reducing transport cost. Imports from a global market will focus on renewable hydrogen-based synthetic fuels.

-

Related

![[Translate to English:] How Argentina can become a renewable hydrogen hub and boost global decarbonisation](/fileadmin/_processed_/8/c/csm_news_4d473bf99c.jpg)