-

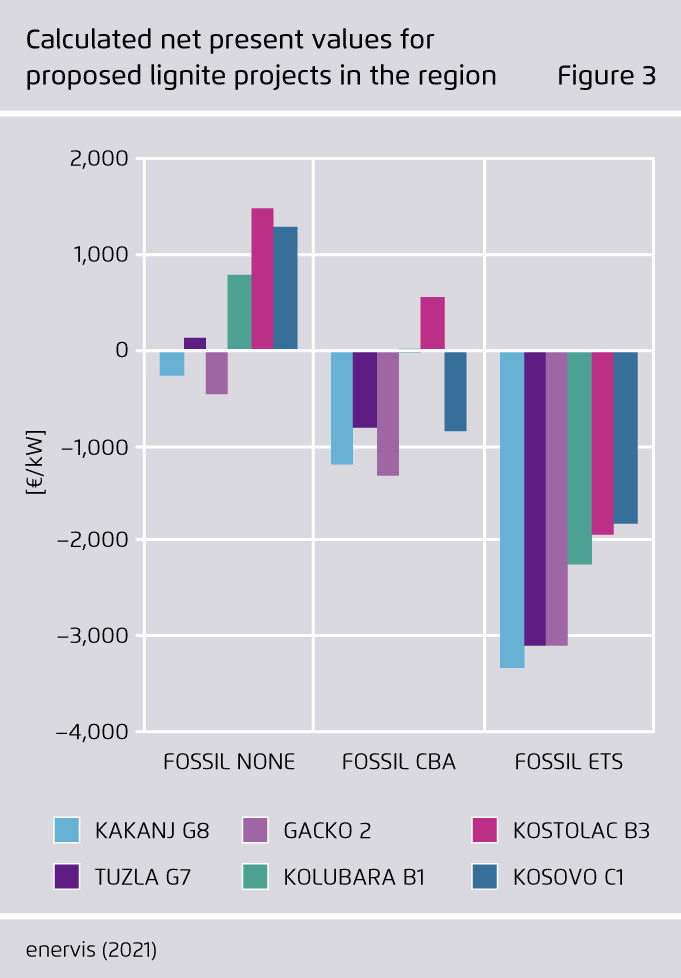

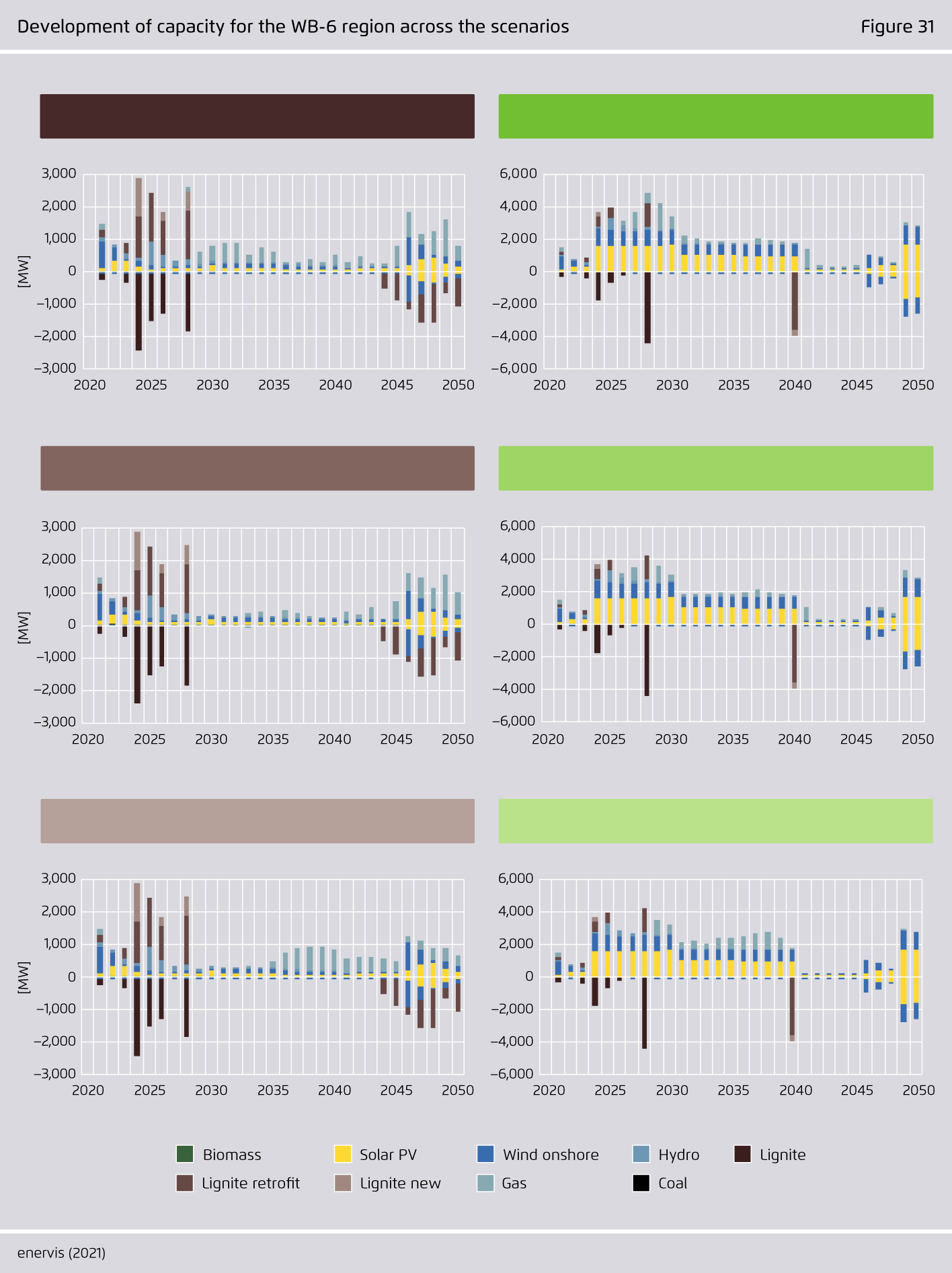

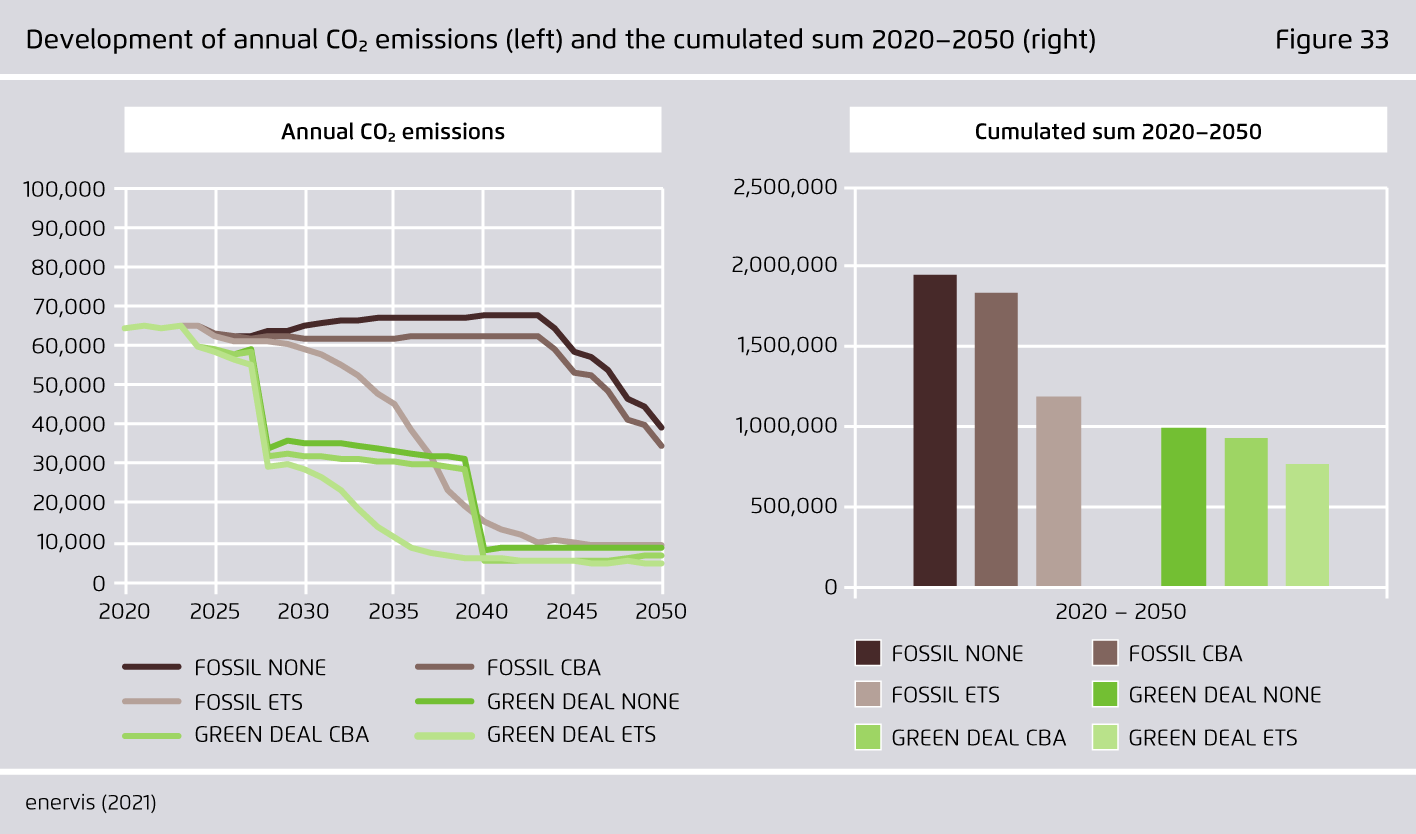

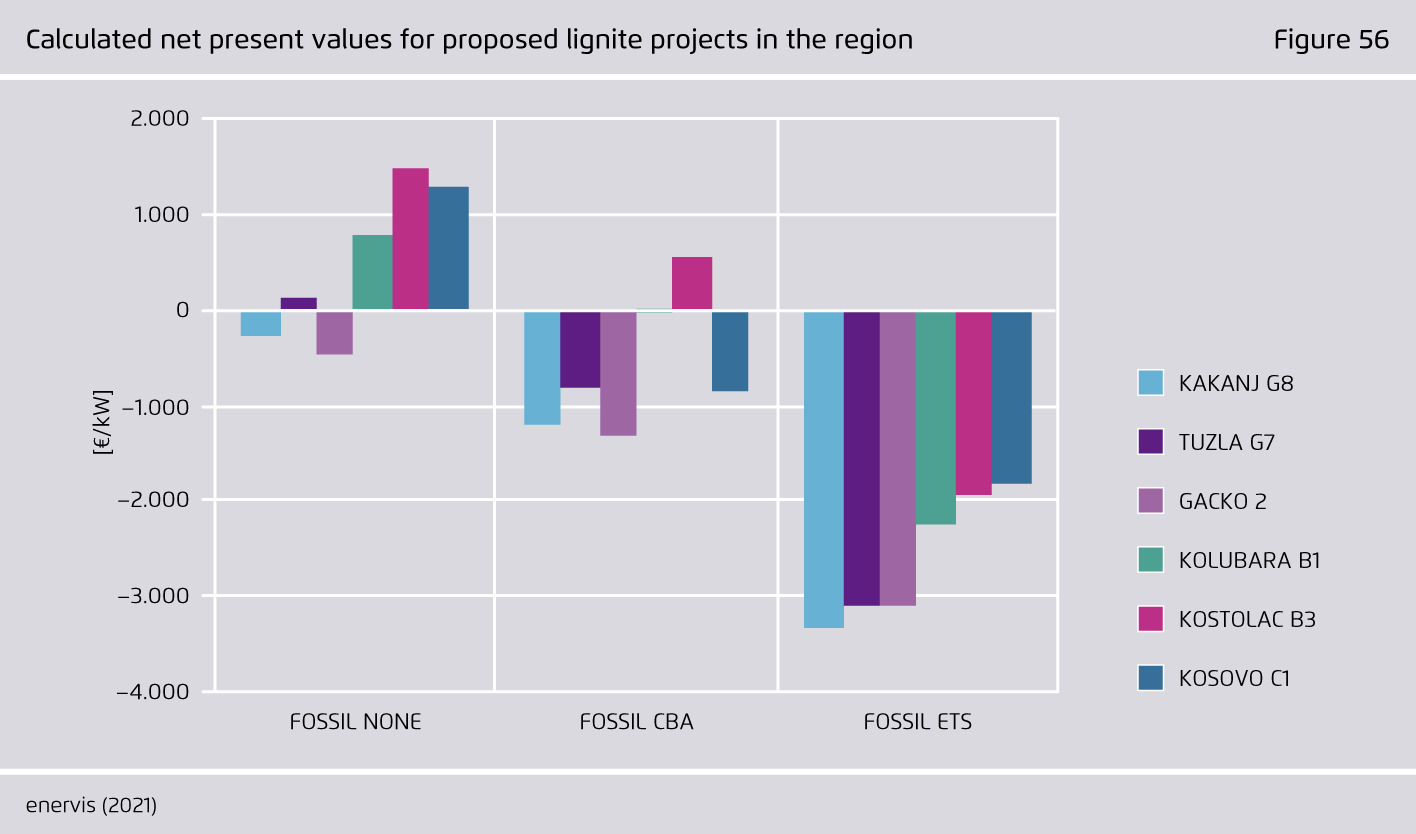

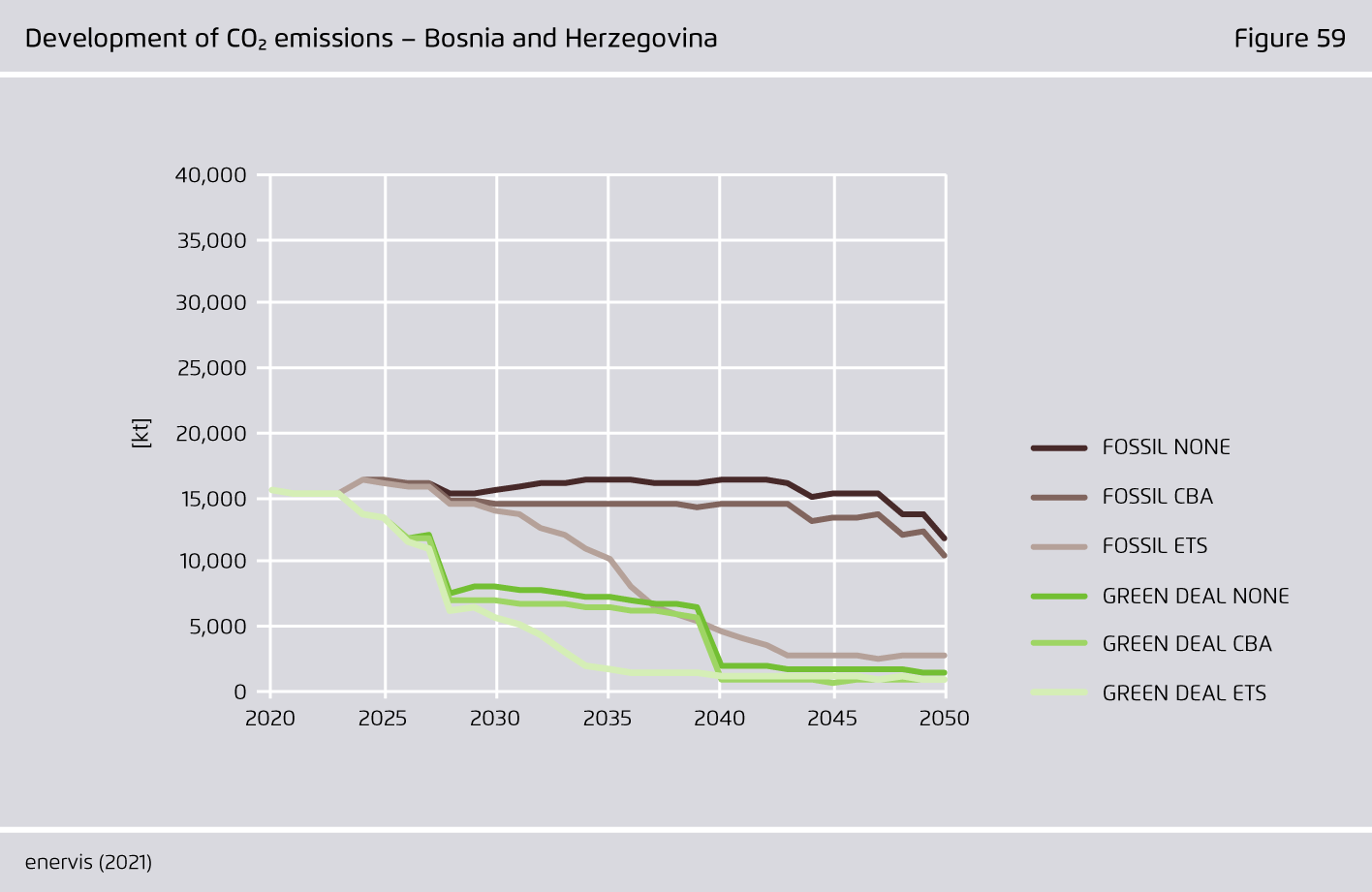

The strong outlook for carbon pricing in the Western Balkans means that new lignite plants will be loss making.

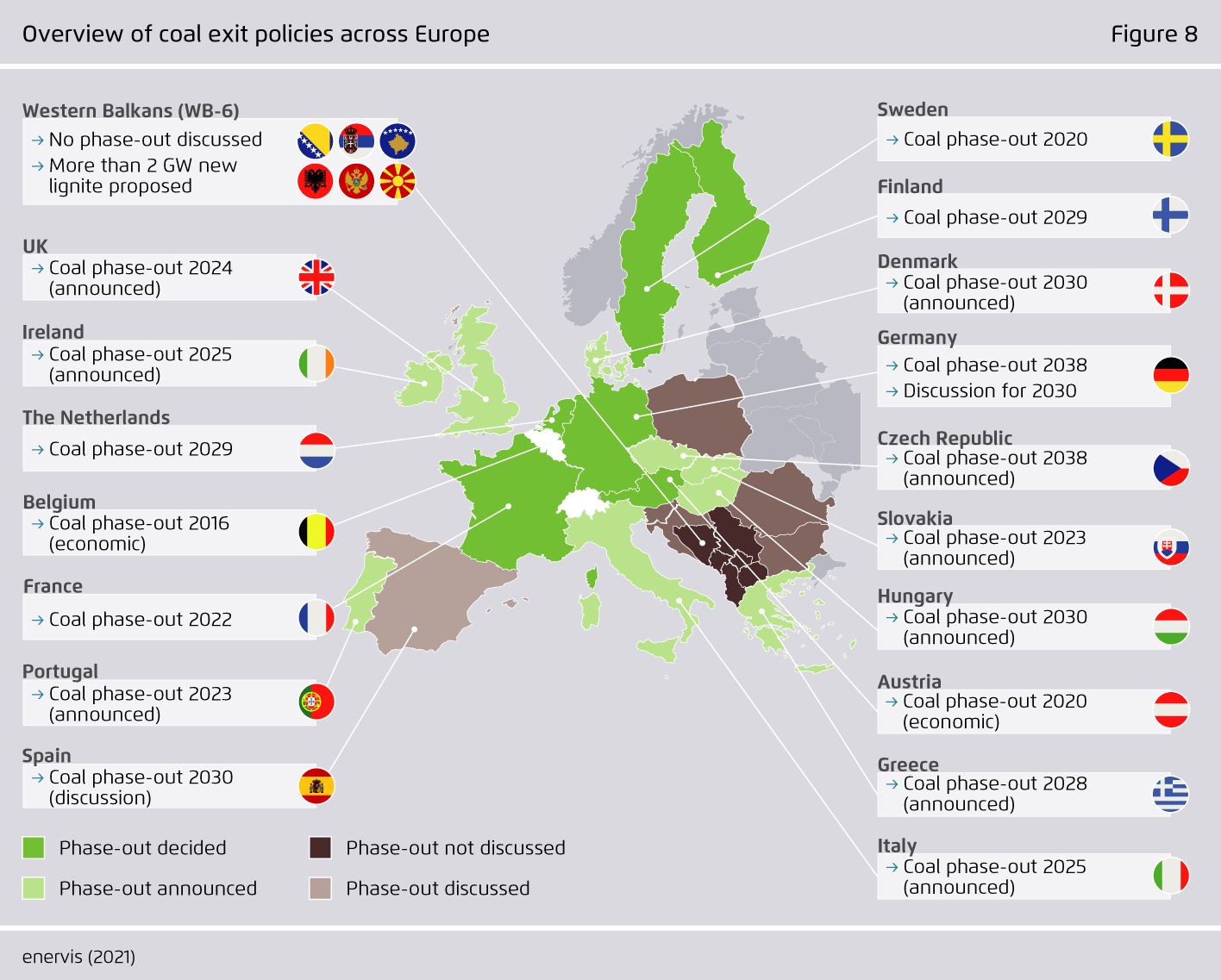

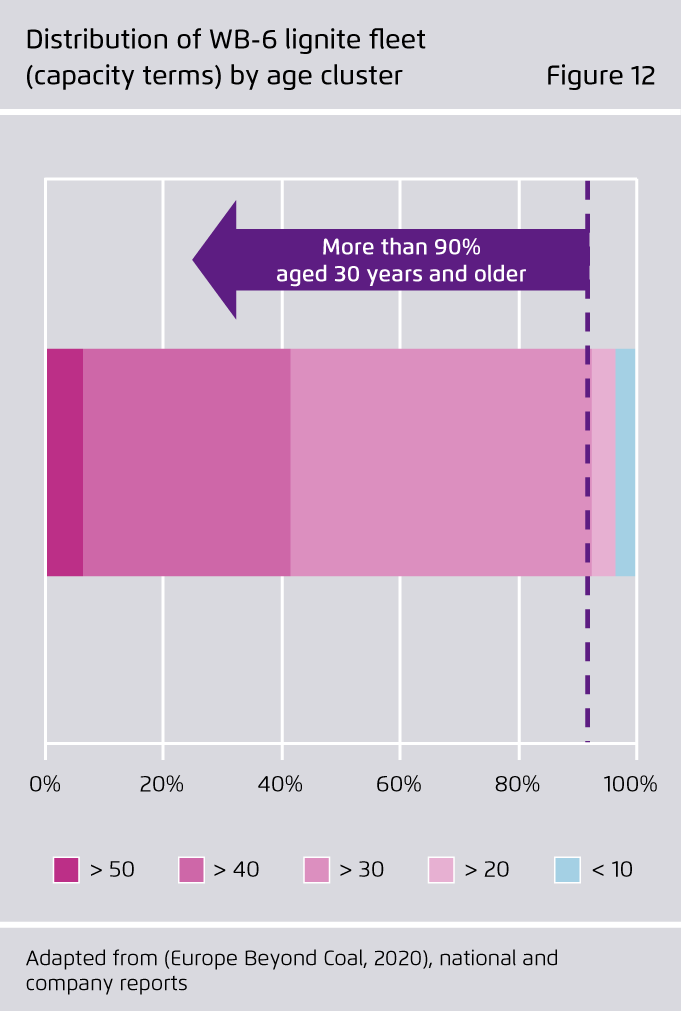

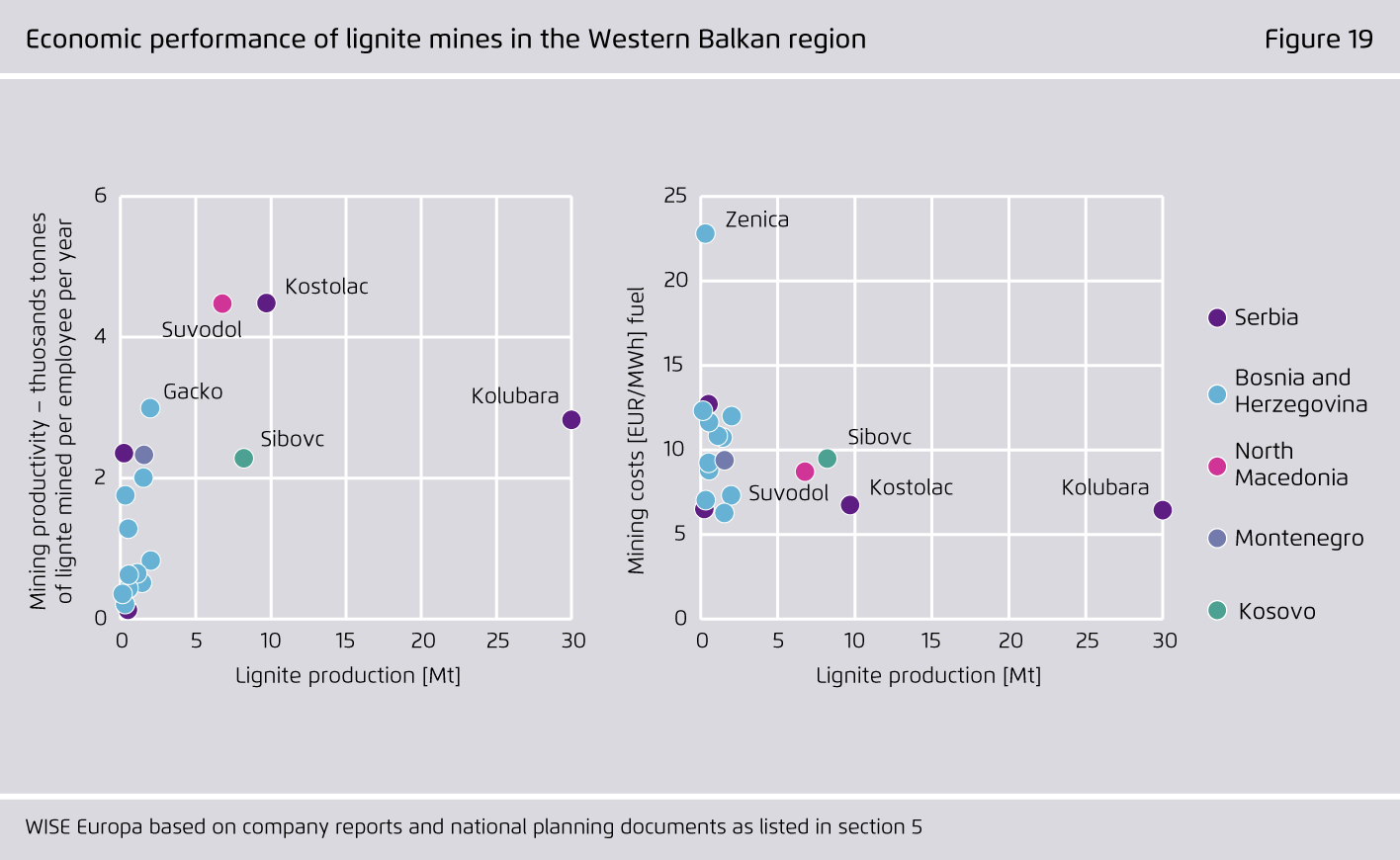

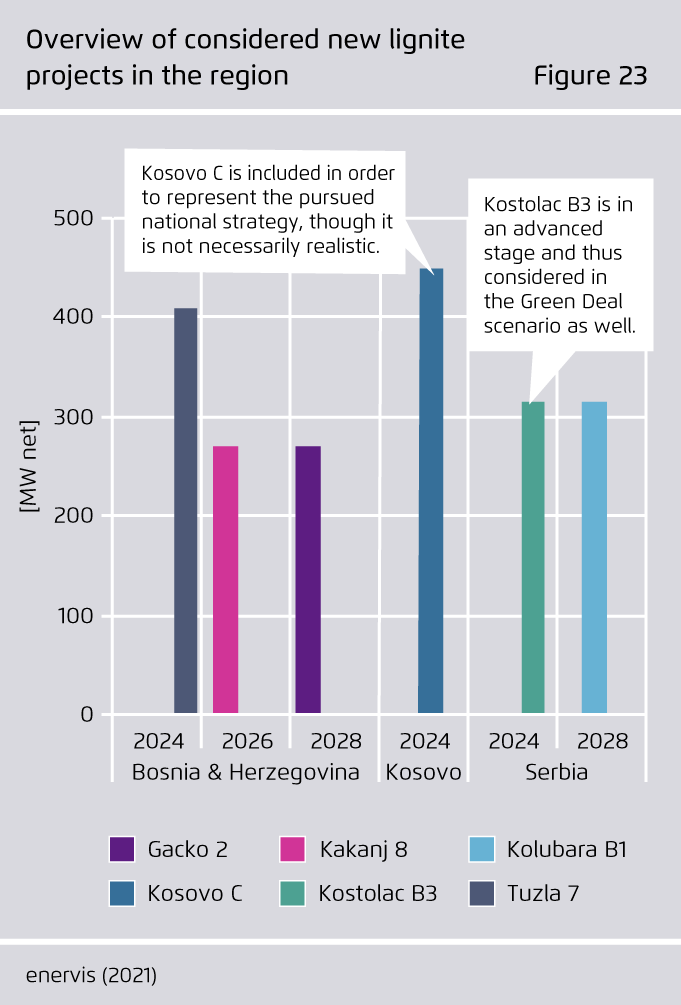

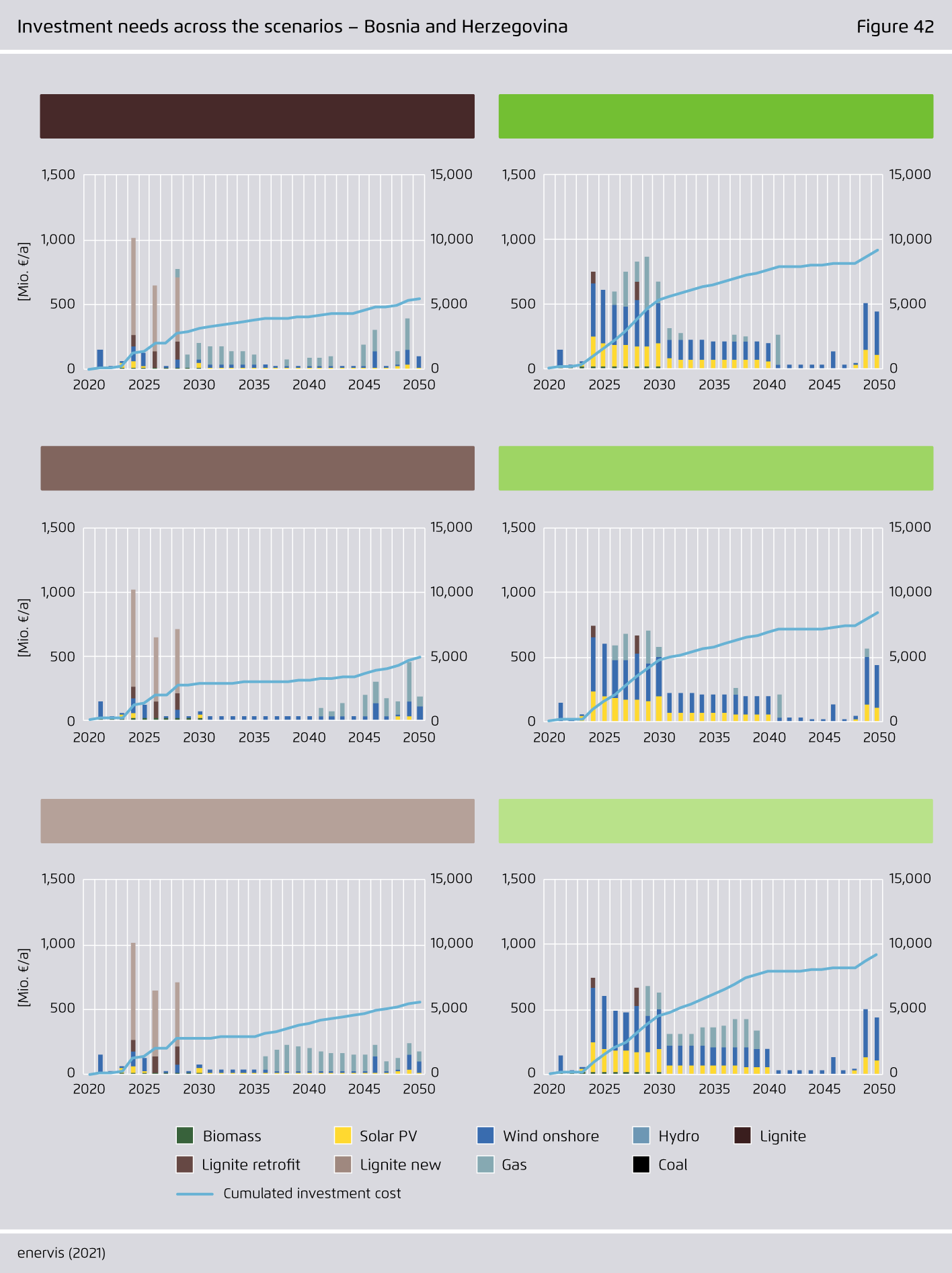

2 GW of new lignite capacity is currently planned in the region. If built, these plants will generate a cumulative loss by 2040. This is because of low efficiency of lignite mining, costs to comply with air pollution regulation and limited export opportunities after establishment of the EU Carbon Border Adjustment Mechanism (CBAM). A phase-in of carbon pricing in Energy Community countries would further increase losses.

-

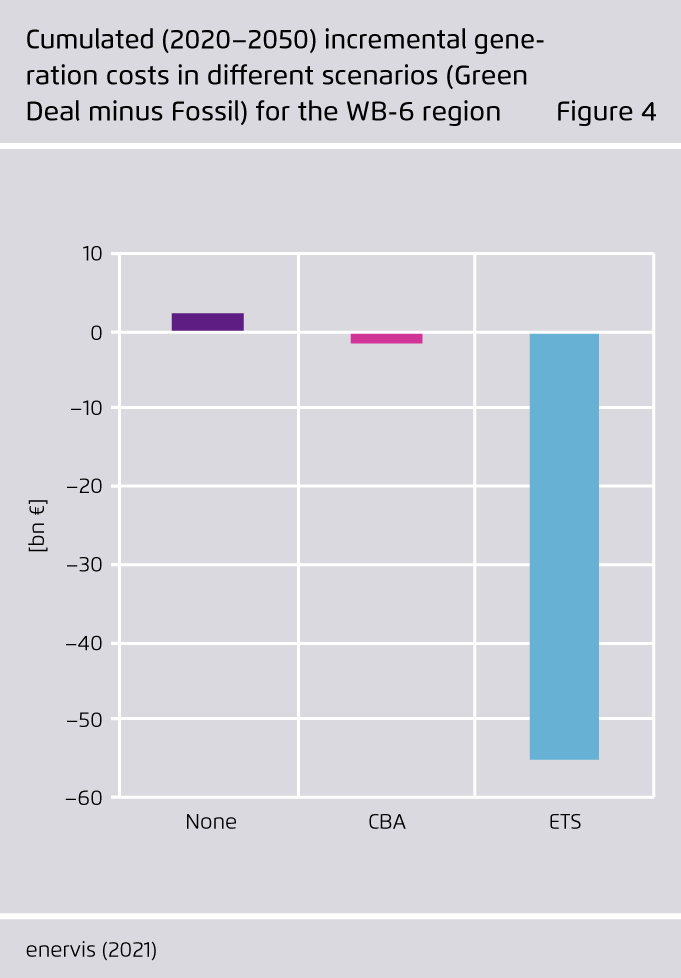

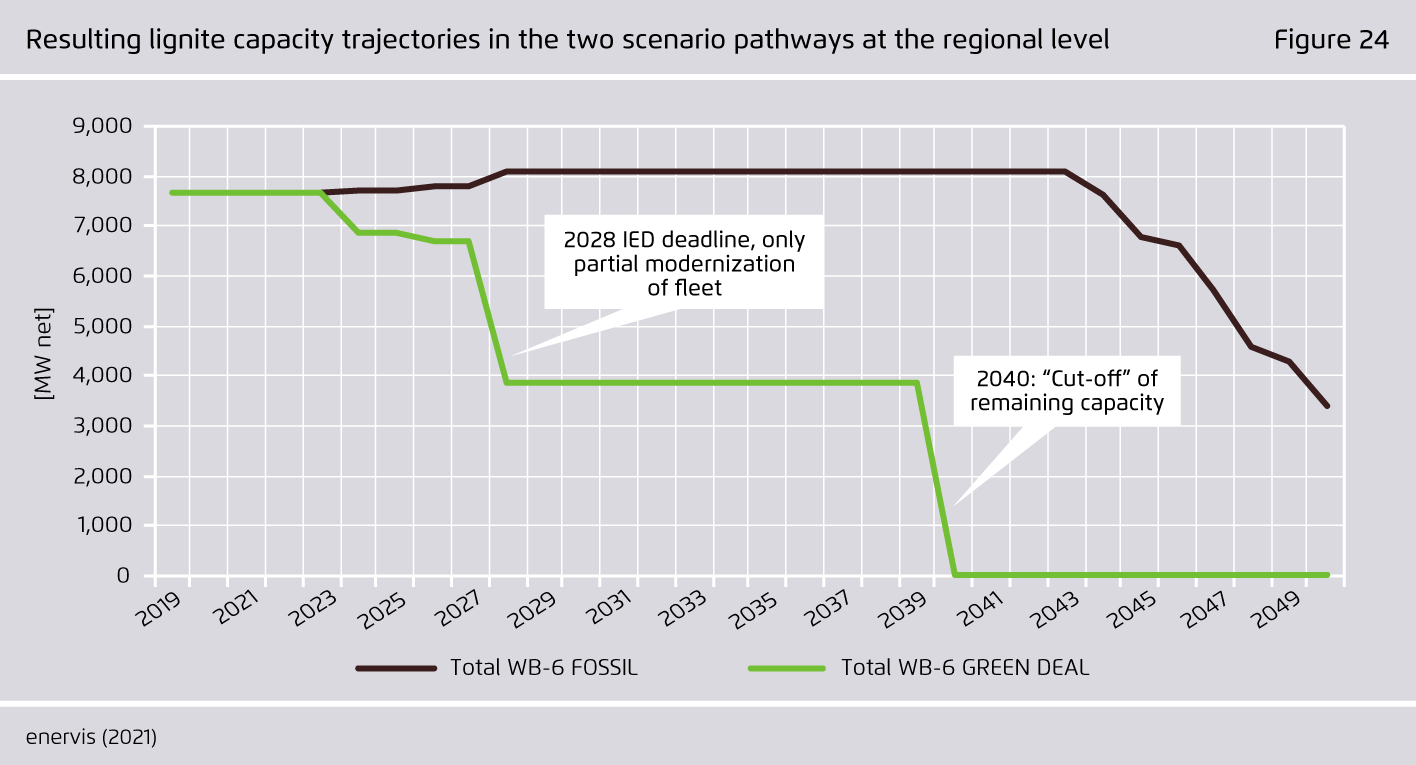

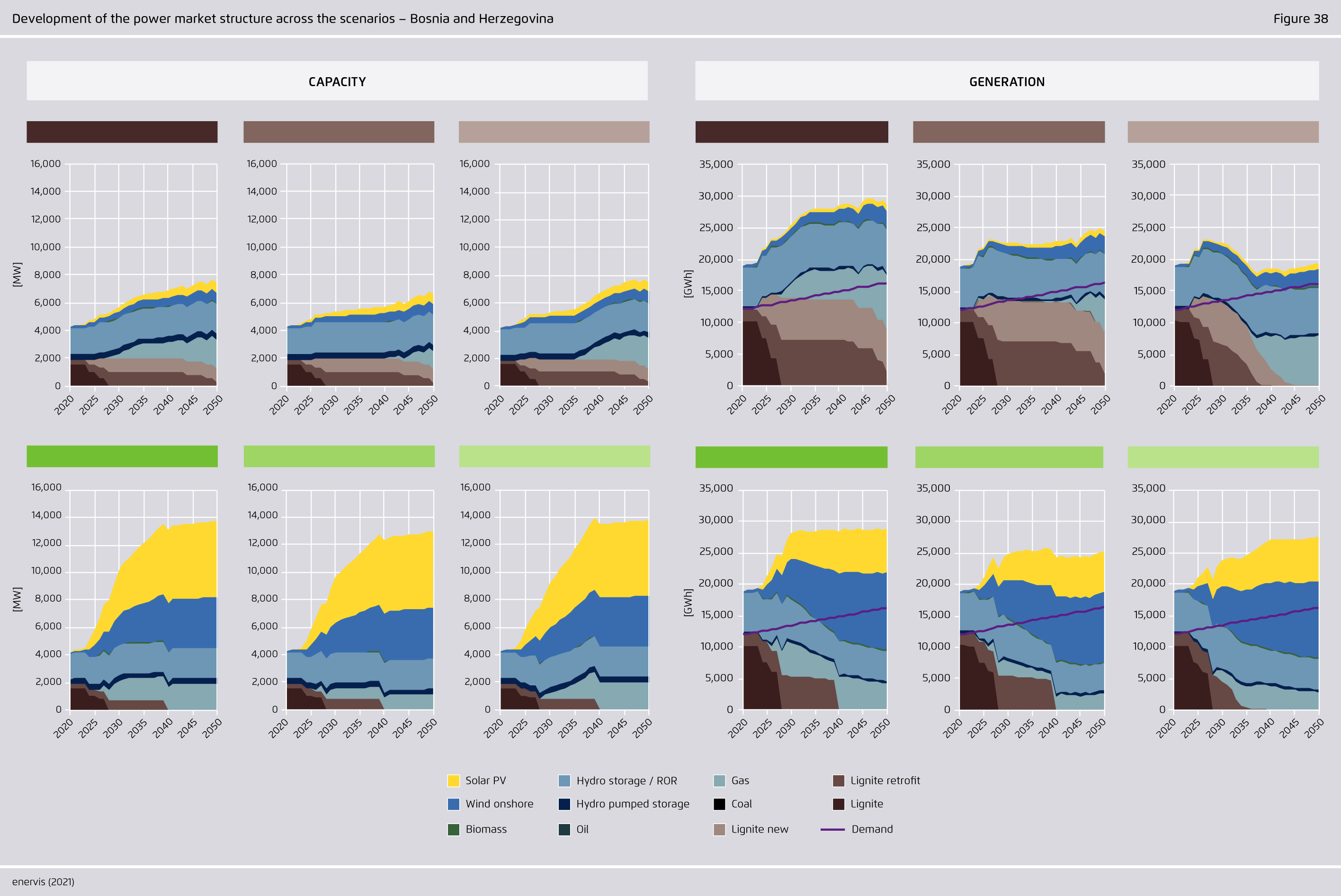

From an economic perspective, existing lignite units in the region should be closed by 2040.

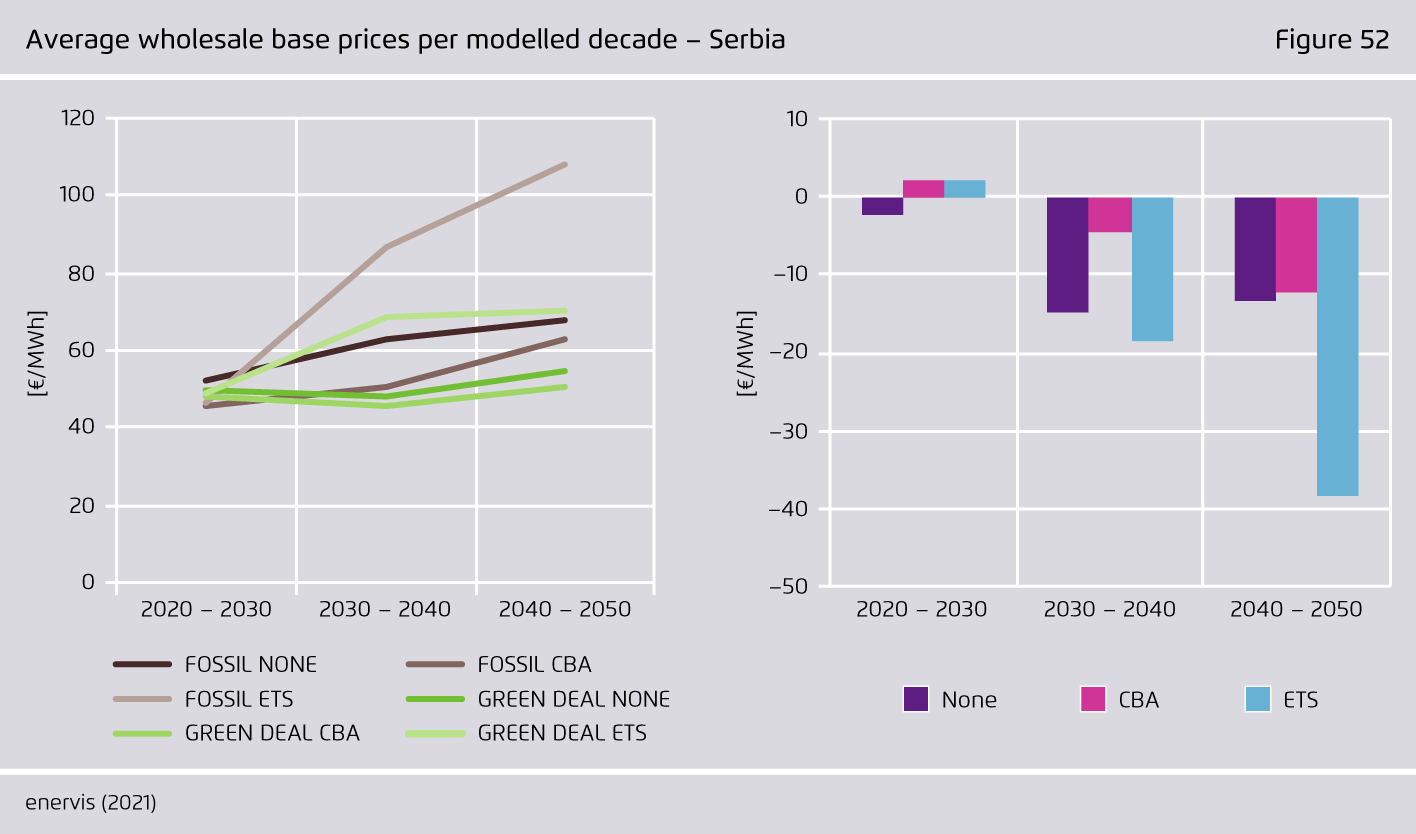

A 2040 lignite exit increases system costs by 3–4 €/MWh in an unlikely scenario without carbon pricing. With the EU CBAM regime or any other form of domestic carbon pricing, closing lignite plants by 2040 lowers system costs.

-

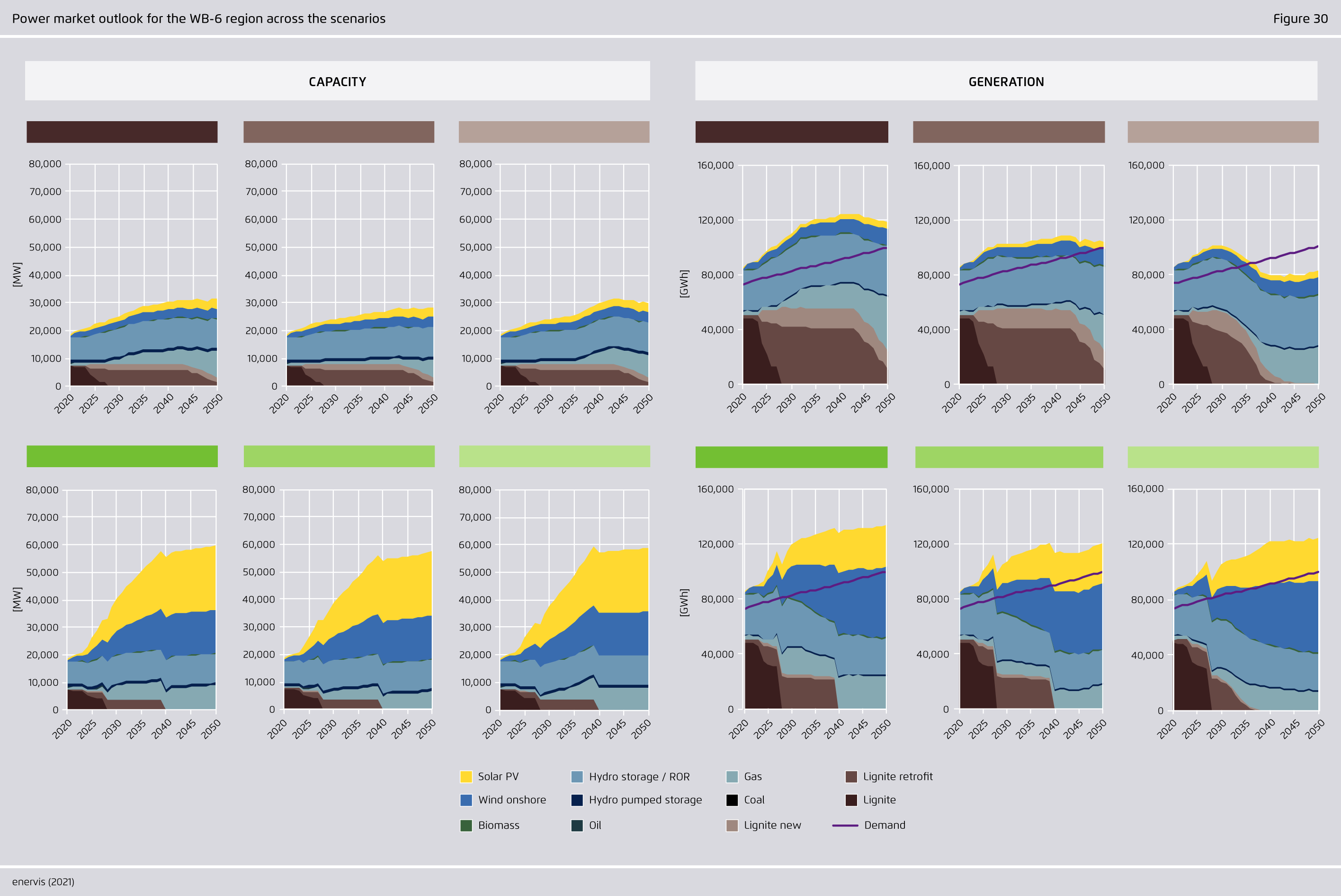

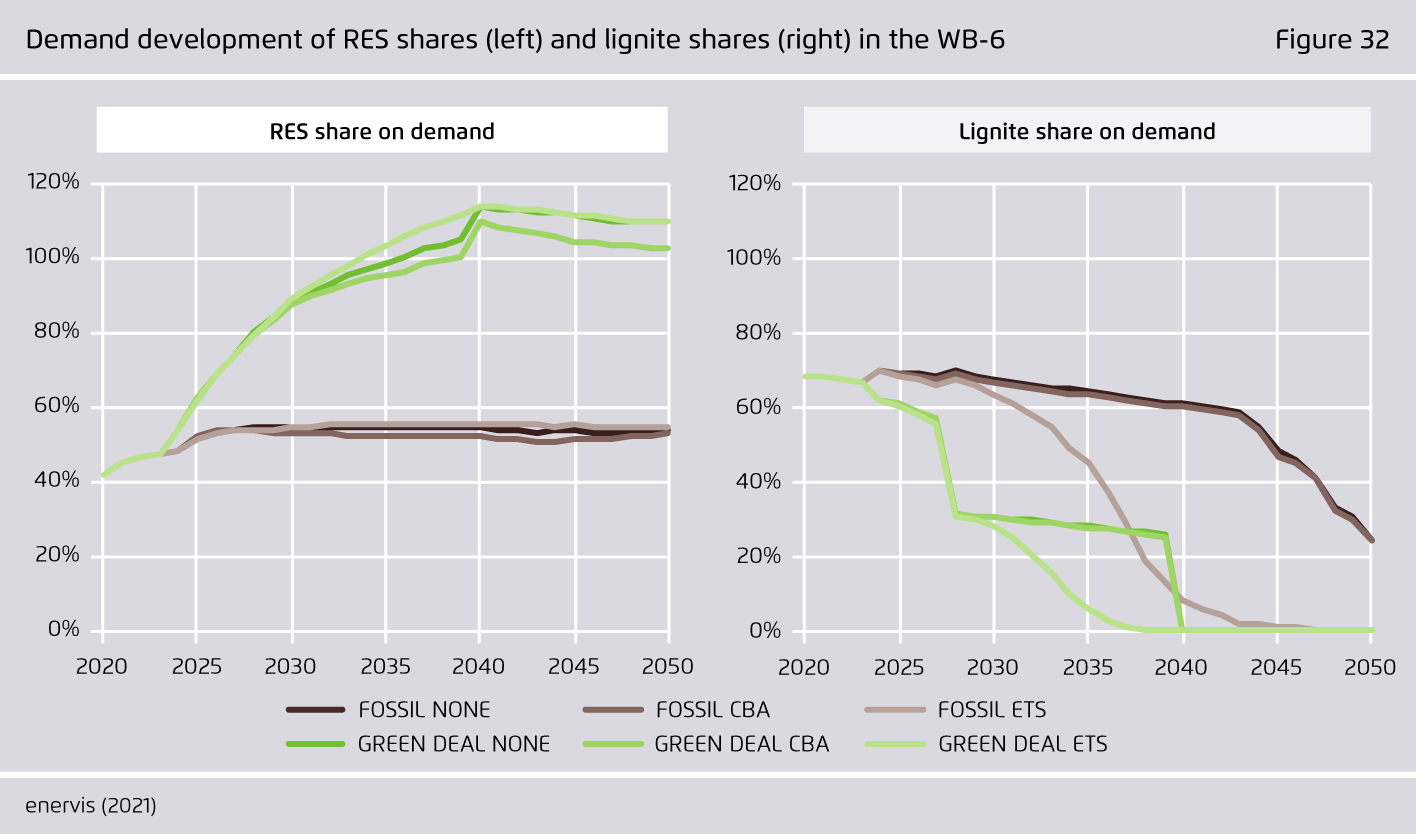

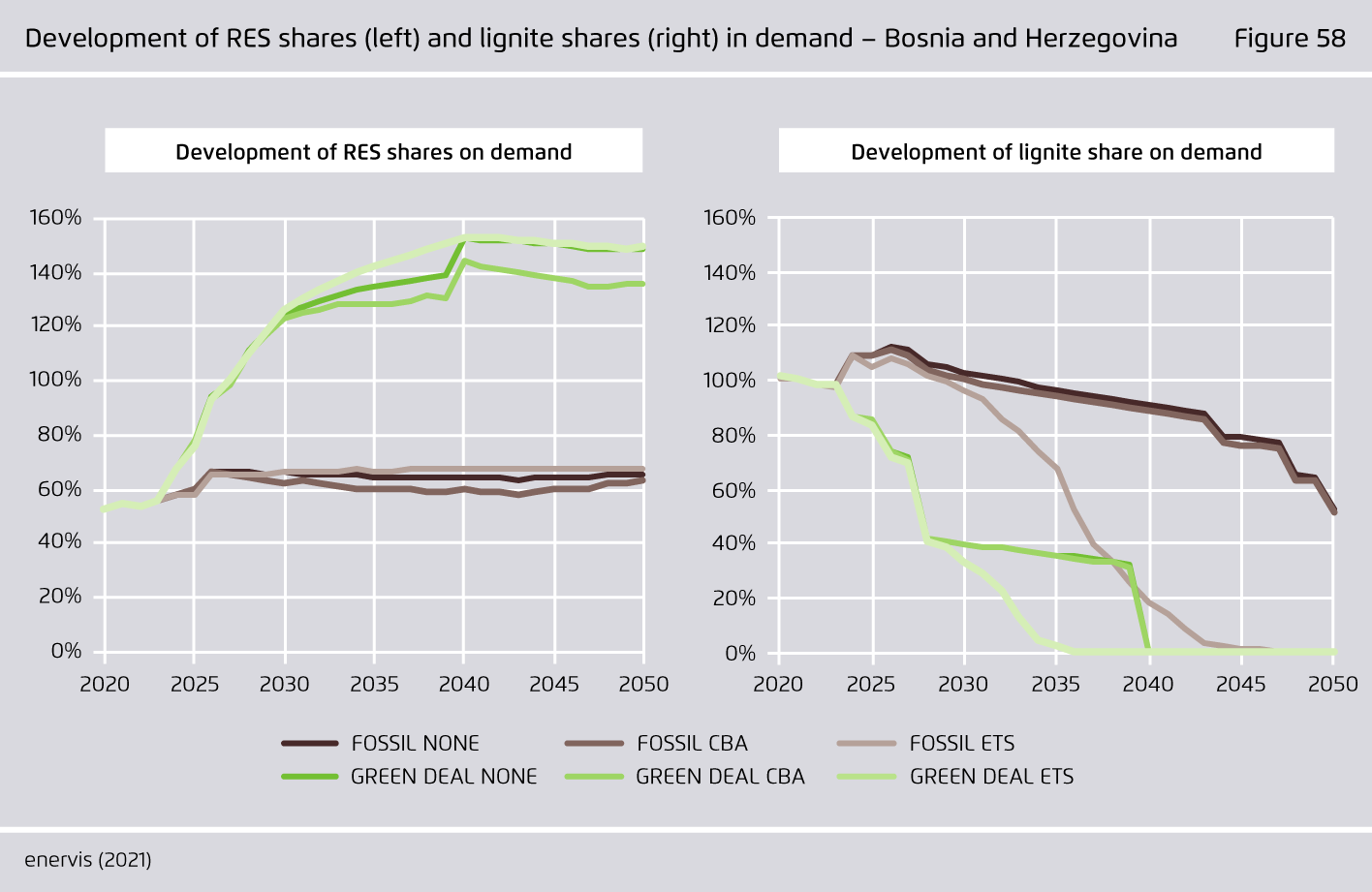

The planned and gradual phase-out of lignite will ensure security of supply.

Security of supply is not an issue if the gradual phase-out of lignite is accompanied by a rapid scaling of renewables, enhanced interconnections, regional power market integration, strengthening of existing hydro-storage and targeted investments in flexible gas plants. Expanding renewables also reduces import dependency of the power and energy sectors.

-

A renewables-based power system is a ‘no regret’ strategy for the Western Balkans.

Replacing lignite generation by renewables lowers wholesale prices, hedges against carbon prices and avoids that fossil gas infrastructure will become stranded. Renewables deployment can largely be financed from market revenues, especially in case of carbon pricing. Renewables also come with many co-benefits such as improved air quality and new job opportunities. ‘Just transition’ policies would ensure that no one is left behind.

-

Related